Cryptocurrency Tax Reporting for 2026: Navigating the Latest IRS Guidelines and Avoiding Common Mistakes

The world of cryptocurrency is dynamic, rapidly evolving, and with its growth comes increased scrutiny from tax authorities worldwide. For investors and enthusiasts in the United States, understanding the intricacies of crypto tax reporting for the 2026 tax year is not just important, it’s absolutely critical. The Internal Revenue Service (IRS) continues to refine its guidance on digital assets, making it imperative for taxpayers to stay informed and compliant. This comprehensive guide will delve into the anticipated IRS guidelines for 2026, highlight common pitfalls to avoid, and provide actionable strategies to ensure your crypto tax reporting is accurate and penalty-free.

The landscape of digital assets has expanded far beyond just Bitcoin and Ethereum. We now see a proliferation of NFTs, DeFi protocols, staking, yield farming, and various other complex transactions. Each of these can have unique tax implications, and the IRS is increasingly sophisticated in its ability to track and identify non-compliance. Ignoring your crypto tax obligations is no longer an option, and the consequences for doing so can be severe, ranging from hefty fines to potential criminal charges.

Our aim is to demystify crypto tax reporting, providing clarity on what constitutes a taxable event, how to accurately calculate gains and losses, and what records you need to keep. By proactively understanding and preparing for the 2026 tax season, you can navigate these complex waters with confidence and ensure you meet all your obligations. Let’s embark on this journey to master your crypto tax reporting.

The Evolving IRS Stance on Cryptocurrency: What to Expect for 2026

The IRS has been progressively tightening its grip on cryptocurrency tax compliance since issuing Notice 2014-21, which classified virtual currency as property for tax purposes. This fundamental classification means that general tax principles applicable to property transactions apply to transactions involving virtual currency. For the 2026 tax year, we anticipate further clarification and potentially new regulations, building upon recent directives and enforcement actions.

Key Areas of IRS Focus

- Increased Data Collection: The IRS is leveraging advanced analytics and partnerships with third-party data providers to identify taxpayers with crypto holdings. Expect more refined reporting requirements from exchanges and custodians.

- DeFi and NFTs: These emerging areas present unique challenges for tax authorities. While specific guidance might still be evolving, the general principle remains: if it generates income or a capital gain, it’s likely taxable.

- Broker Reporting: The Infrastructure Investment and Jobs Act (IIJA) of 2021 included provisions for digital asset brokers to report certain transactions to the IRS, similar to how traditional financial institutions report stock trades. While the effective date for these provisions has been pushed back, the underlying intent for increased transparency and reporting is clear and will significantly impact crypto tax reporting in the coming years. Taxpayers should anticipate these changes to be fully implemented and affecting their 2026 tax filings.

- Staking and Mining Income: The IRS views income from staking rewards and crypto mining as ordinary income, taxable at its fair market value at the time it is received. This area has seen some legal challenges, but the IRS’s position has largely held.

- Foreign Crypto Accounts: For those holding crypto on foreign exchanges or in foreign wallets, FBAR (Foreign Bank and Financial Accounts Report) and FATCA (Foreign Account Tax Compliance Act) rules may apply, adding another layer of complexity to crypto tax reporting.

Anticipated Regulatory Changes

While specific new legislation for 2026 is yet to be finalized, taxpayers should monitor announcements from the Treasury Department and the IRS. The trend points towards greater standardization of reporting, increased enforcement, and potentially more specific guidance for complex DeFi activities. The goal is to close the ‘tax gap’ – the difference between taxes owed and taxes paid – in the digital asset space.

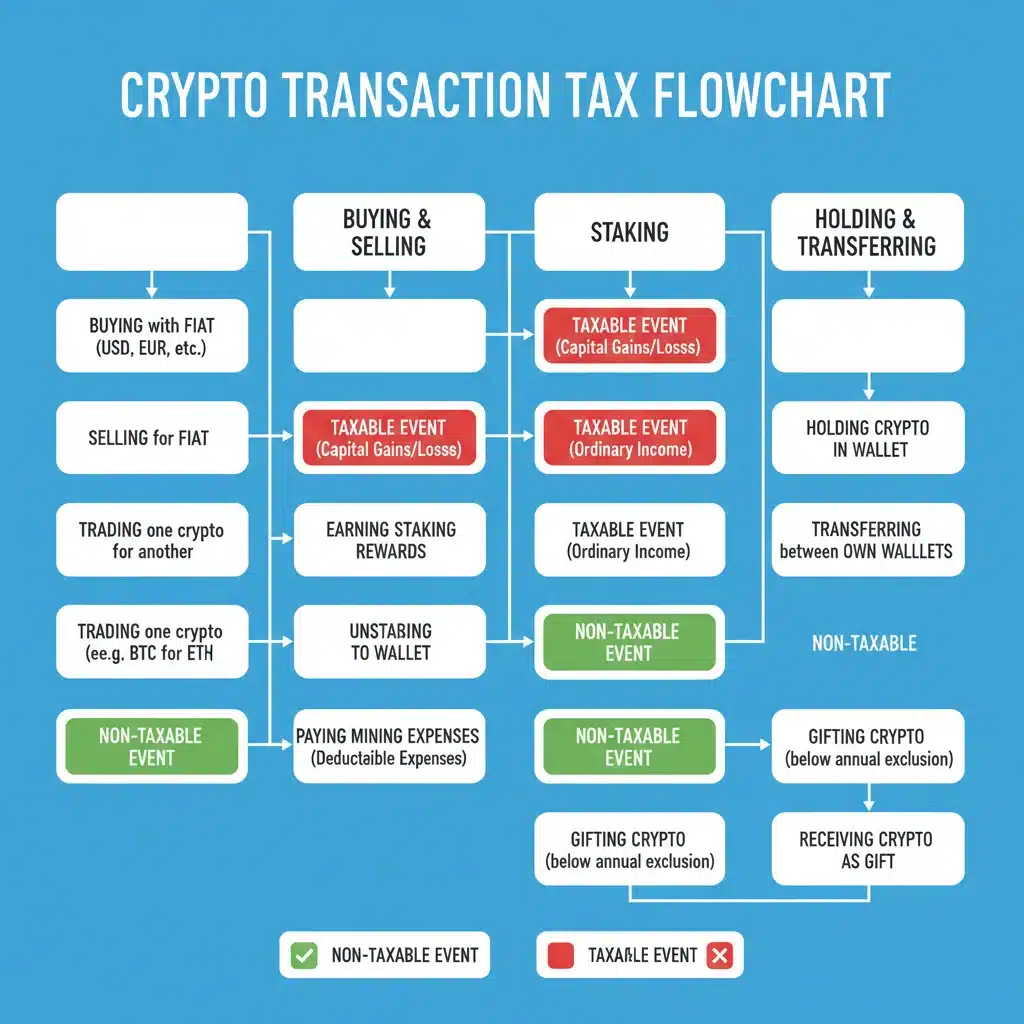

Understanding Taxable Events in Cryptocurrency

A crucial first step in accurate crypto tax reporting is identifying what constitutes a taxable event. Unlike traditional fiat currency, nearly every interaction with cryptocurrency can trigger a tax implication. Here’s a breakdown:

Sales and Exchanges

When you sell cryptocurrency for fiat currency (e.g., USD) or exchange one cryptocurrency for another (e.g., Bitcoin for Ethereum), it is considered a taxable event. The gain or loss is calculated based on the difference between the fair market value of the crypto at the time of disposition and its cost basis (what you paid for it).

Using Crypto for Goods and Services

Paying for goods or services with cryptocurrency is also a taxable event. The IRS views this as selling your crypto for its fair market value, and then using that ‘cash’ to make a purchase. You’ll realize a capital gain or loss on the crypto used.

Mining and Staking Rewards

Income derived from mining new cryptocurrency or receiving rewards from staking is generally considered ordinary income. This income is taxable at its fair market value at the time you receive it. The cost basis for this newly acquired crypto then becomes that fair market value.

Airdrops and Hard Forks

Receiving cryptocurrency via an airdrop or a hard fork can also be a taxable event. If you have dominion and control over the new crypto, its fair market value at the time of receipt is typically considered ordinary income.

Gifts and Donations

Giving cryptocurrency as a gift may have gift tax implications, though there’s usually a generous annual exclusion amount. Donating crypto to a qualified charity can be tax-deductible, similar to donating appreciated stock.

Initial Coin Offerings (ICOs) and Initial Exchange Offerings (IEOs)

Participating in ICOs or IEOs involves purchasing tokens, which establishes your cost basis. Subsequent sales or exchanges of these tokens will trigger capital gains or losses.

Calculating Gains and Losses: The Foundation of Accurate Crypto Tax Reporting

Accurately calculating capital gains and losses is the cornerstone of effective crypto tax reporting. This involves understanding cost basis, holding periods, and different accounting methods.

Cost Basis

Your cost basis is essentially what you paid for your cryptocurrency, including any fees or commissions. It’s crucial to track this for every unit of crypto you acquire.

Holding Periods: Short-Term vs. Long-Term

- Short-Term Capital Gains/Losses: Apply to crypto held for one year or less. These gains are taxed at your ordinary income tax rates.

- Long-Term Capital Gains/Losses: Apply to crypto held for more than one year. These gains are taxed at more favorable long-term capital gains rates (0%, 15%, or 20% depending on your income bracket).

Understanding the holding period is vital for tax optimization. Strategic holding can significantly reduce your tax liability.

Accounting Methods for Cost Basis

When you sell only a portion of your crypto holdings, and you’ve acquired that crypto at different times and prices, you need a method to determine which specific units you’re selling. The IRS allows two primary methods:

- Specific Identification: This is the most advantageous method. It allows you to choose which specific units of crypto you are selling (e.g., those with the highest cost basis to minimize gains, or those held for over a year to qualify for long-term rates). To use this method, you must be able to identify the specific units sold, their purchase date, and their cost basis.

- First-In, First-Out (FIFO): This method assumes that the first cryptocurrency you acquired is the first one you sell. While simpler, it might not always be the most tax-efficient, as it can result in higher capital gains if the price of your crypto has generally increased over time.

It’s important to choose an accounting method and apply it consistently. Most crypto tax software can help manage these calculations.

Common Mistakes in Crypto Tax Reporting and How to Avoid Them

Even with the best intentions, taxpayers often make mistakes when dealing with crypto tax reporting. Being aware of these common pitfalls can help you steer clear of IRS scrutiny.

1. Underreporting or Failing to Report All Transactions

Mistake: Many taxpayers only report transactions where they converted crypto back to fiat, overlooking crypto-to-crypto trades, spending crypto, or income from staking/mining.

Solution: Track every single crypto transaction, regardless of its nature. Use crypto tax software or meticulously maintain your own records from all exchanges and wallets.

2. Incorrectly Calculating Cost Basis

Mistake: Not including transaction fees in the cost basis, or misidentifying the cost basis for specific units, especially when using different exchanges or wallets.

Solution: Keep detailed records of all purchases, including the date, amount, price, and any associated fees. Leverage specific identification for optimal tax outcomes if your records allow.

3. Confusing Gifts with Income

Mistake: Receiving crypto as a gift and mistakenly treating it as income, or vice-versa, leading to incorrect tax calculations.

Solution: Understand the distinction. Gifts are generally not taxable to the recipient, but the donor might have gift tax obligations. Income (like airdrops, staking rewards) is taxable to the recipient.

4. Ignoring Foreign Account Reporting Requirements (FBAR/FATCA)

Mistake: Failing to report foreign crypto accounts if their aggregate value exceeds certain thresholds.

Solution: If you hold crypto on non-U.S. exchanges or in foreign wallets, be aware of FBAR and FATCA requirements. Consult a tax professional if you have foreign assets.

5. Neglecting Record-Keeping

Mistake: Not maintaining comprehensive records of all crypto transactions, making it impossible to accurately calculate gains/losses or prove compliance during an audit.

Solution: Implement a robust record-keeping system from day one. This includes transaction IDs, dates, fair market values, wallet addresses, and exchange statements. Many crypto tax software solutions automate this process.

6. Misunderstanding Wash Sale Rules

Mistake: Applying traditional wash sale rules to crypto. Currently, the IRS does not apply wash sale rules to cryptocurrencies because they are classified as property, not securities. However, this could change. Some taxpayers mistakenly believe they cannot harvest losses if they repurchase the same crypto within 30 days.

Solution: For the 2026 tax year, you can still harvest crypto losses even if you buy back the same asset shortly after. However, always stay updated on potential legislative changes that could introduce wash sale rules for digital assets.

7. Not Seeking Professional Help When Needed

Mistake: Attempting to navigate complex crypto tax situations without the guidance of a qualified tax professional.

Solution: If your crypto activities are extensive or complex (e.g., significant DeFi involvement, multiple NFTs, large trading volumes), consult a tax advisor specializing in digital assets. Their expertise can save you time, stress, and potential penalties.

Essential Tools and Strategies for Seamless Crypto Tax Reporting

Effective crypto tax reporting doesn’t have to be a nightmare. With the right tools and strategies, you can streamline the process and ensure accuracy.

1. Utilize Crypto Tax Software

These platforms are invaluable for tracking transactions across multiple exchanges and wallets, calculating cost basis, and generating necessary tax forms (like Form 8949). Popular options include:

- CoinTracker

- Koinly

- TaxBit

- Accointing

These tools integrate with most major exchanges via API, import CSV files, and can handle complex transactions like staking, mining, and DeFi. They are designed to simplify the aggregation of data and the calculation of capital gains and ordinary income.

2. Maintain Meticulous Records

Even with software, manual record-keeping for certain transactions or sanity checks can be beneficial. Keep a detailed spreadsheet or log that includes:

- Date and time of each transaction.

- Type of transaction (buy, sell, trade, gift, receive, spend, stake, mine).

- Cryptocurrency involved (e.g., BTC, ETH).

- Quantity of crypto.

- Fiat value at the time of the transaction.

- Associated fees.

- Wallet addresses or exchange names.

- Purpose of the transaction (e.g., purchase of XYZ NFT).

3. Understand DeFi and NFT Tax Implications

Decentralized Finance (DeFi) and Non-Fungible Tokens (NFTs) introduce new layers of complexity. For DeFi, activities like liquidity providing, yield farming, and borrowing/lending can generate taxable income or trigger taxable events. For NFTs, buying and selling are capital events, while creating (minting) an NFT can have income implications if royalties are earned.

It’s crucial to track the fair market value of tokens received in DeFi protocols at the time of receipt and to record the cost basis of NFTs. Specialized tax software often has features to help categorize these transactions, but expert advice is often recommended for complex scenarios.

4. Tax Loss Harvesting

This is a powerful strategy to reduce your overall tax liability. If you have capital gains from crypto or other investments, you can sell depreciated crypto assets to realize capital losses. These losses can then offset capital gains. If your capital losses exceed your capital gains, you can deduct up to $3,000 of ordinary income per year, carrying forward any remaining losses to future tax years.

As mentioned, for 2026, crypto is not subject to wash sale rules, offering more flexibility for tax loss harvesting compared to traditional securities. However, always confirm the latest IRS guidance.

5. Engage with Tax Professionals

For significant crypto holdings or complex investment strategies, engaging a tax professional experienced in digital assets is highly advisable. They can provide personalized advice, ensure compliance with the latest regulations, and help optimize your tax strategy.

What Forms Do You Need for Crypto Tax Reporting?

When it comes to crypto tax reporting, several IRS forms may come into play, depending on your activities:

Form 8949, Sales and Other Dispositions of Capital Assets

This is the primary form for reporting capital gains and losses from selling or exchanging cryptocurrency. Each taxable event (sale, exchange, spending crypto) needs to be listed here. Crypto tax software is invaluable for generating this form accurately.

Schedule D, Capital Gains and Losses

The totals from Form 8949 are then transferred to Schedule D, where your net capital gain or loss is calculated and reported on your Form 1040.

Schedule 1 (Form 1040), Additional Income and Adjustments to Income

Income from staking rewards, mining, airdrops, and other similar activities is generally reported as ‘Other Income’ on Schedule 1.

Form 1040, U.S. Individual Income Tax Return

All your income, deductions, and credits, including those related to cryptocurrency, ultimately consolidate on your main Form 1040.

FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR)

If the aggregate value of your foreign crypto accounts exceeds $10,000 at any point during the year, you may be required to file an FBAR with the Financial Crimes Enforcement Network (FinCEN). While the IRS has clarified that virtual currencies are not currency for FBAR purposes, some interpretations still suggest reporting is prudent, especially if held in a custodial account that also holds traditional currency. It’s an area that still warrants careful attention and professional advice.

Form 8938, Statement of Specified Foreign Financial Assets

Similar to FBAR, this form is required for certain U.S. taxpayers who have an interest in specified foreign financial assets with an aggregate value exceeding certain thresholds. This could include foreign crypto holdings.

The Importance of Proactive Compliance

The IRS is not slowing down its efforts to ensure compliance in the digital asset space. They have issued ‘soft notices’ to taxpayers they suspect of underreporting crypto income, conducted audits, and utilized data from various sources to identify non-compliant individuals. Proactive compliance is your best defense against penalties and legal issues.

By understanding the rules, diligently tracking your transactions, utilizing appropriate software, and seeking professional advice when necessary, you can confidently navigate the complexities of crypto tax reporting for 2026 and beyond. Don’t wait until tax season to start gathering your information; begin now to ensure a smooth and accurate filing process.

Future Outlook for Crypto Tax Reporting

The regulatory landscape for cryptocurrency is still evolving, and 2026 will likely be another year of significant developments. We can expect continued efforts from the IRS to:

- Clarify DeFi and NFT Taxation: As these sectors mature, more specific guidance on how to report complex transactions like liquidity pool farming, flash loans, and fractionalized NFTs is anticipated.

- Enhance Broker Reporting: The full implementation of broker reporting requirements, as mandated by the IIJA, will provide the IRS with unprecedented visibility into cryptocurrency transactions. This will significantly reduce the ability to underreport or omit crypto activities without detection.

- International Cooperation: Tax authorities globally are collaborating more to share information on digital asset transactions, making it harder for individuals to use international exchanges to evade taxes.

- Focus on Education and Enforcement: The IRS will likely continue its two-pronged approach of educating taxpayers about their obligations while simultaneously increasing enforcement actions against those who willfully disregard tax laws.

Staying informed about these potential changes is part of a robust compliance strategy. Subscribing to tax news, attending webinars, and consulting with tax professionals are excellent ways to remain updated.

Conclusion: Master Your Crypto Tax Reporting for 2026

Navigating crypto tax reporting for 2026 requires diligence, attention to detail, and a clear understanding of the IRS’s evolving guidelines. The digital asset space is complex, but by taking a proactive approach, you can ensure compliance and avoid unnecessary stress or penalties. Remember to:

- Track Every Transaction: From buying and selling to staking and spending, every crypto interaction matters.

- Understand Taxable Events: Identify when you incur capital gains/losses or ordinary income.

- Maintain Thorough Records: Your transaction history is your most valuable asset during tax season.

- Leverage Technology: Crypto tax software can significantly simplify the reporting process.

- Seek Expert Advice: Don’t hesitate to consult a tax professional specializing in digital assets for complex situations.

By following these principles, you can confidently approach the 2026 tax season, fulfill your obligations, and continue to participate in the exciting world of cryptocurrency without fear of tax repercussions. The future of finance is digital, and with proper planning, your tax strategy can be just as forward-thinking.

in 2026: A Comprehensive Guide")