Student Loan Policy 2026: Legislative Changes & Borrower Impact

The landscape of higher education finance is perpetually in flux, and nowhere is this more evident than in the realm of student loans. As we approach 2026, a confluence of economic factors, political shifts, and societal demands is poised to shape the future of Student Loan Policy 2026. For millions of current and prospective borrowers, understanding these potential changes is not merely an academic exercise; it’s a critical step in financial planning and navigating the complexities of educational debt.

The sheer volume of outstanding student loan debt in the United States—currently exceeding $1.7 trillion—underscores the profound impact that any policy adjustment can have. This includes federal loan programs, private lending, and various repayment and forgiveness initiatives. The year 2026 is particularly significant as it marks a point where many current pandemic-era relief measures will have concluded, and new legislative priorities may have taken root. This article delves deep into the anticipated legislative changes, their potential implications for borrowers, and strategies to prepare for the evolving financial environment.

The Current State of Student Loan Policy: A Foundation for Change

Before we project into 2026, it’s essential to grasp the current framework of student loan policy. The past few years have seen significant interventions, primarily in response to the economic disruptions caused by the COVID-19 pandemic. These included widespread payment pauses, interest rate freezes on federal loans, and various attempts at targeted debt relief. While many of these measures have expired or are in the process of phasing out, their existence has sparked broader conversations about the sustainability and equity of the student loan system.

Key components of the current system include:

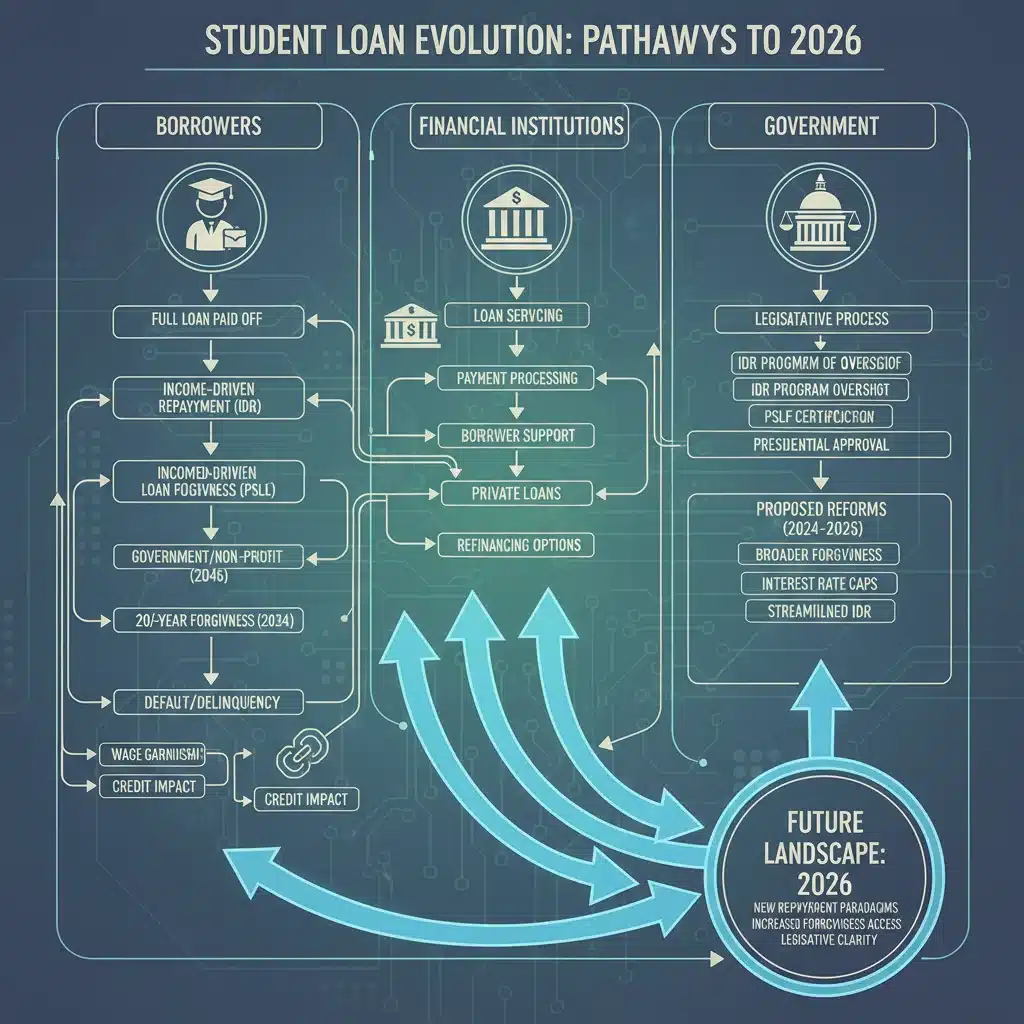

- Federal Student Loans: Dominated by Direct Loans, these offer various repayment plans (Standard, Graduated, Extended, Income-Driven Repayment – IDR), deferment, forbearance, and eligibility for forgiveness programs like Public Service Loan Forgiveness (PSLF).

- Private Student Loans: Offered by banks and private lenders, these typically have fewer borrower protections and less flexible repayment options compared to federal loans.

- Income-Driven Repayment (IDR) Plans: These plans adjust monthly payments based on a borrower’s income and family size, often leading to loan forgiveness after 20 or 25 years of payments. Recent administrative actions have aimed to improve the efficiency and accessibility of IDR plans.

- Public Service Loan Forgiveness (PSLF): A program designed to forgive the remaining balance on Direct Loans for borrowers who work full-time for qualifying non-profit or government organizations and make 120 qualifying monthly payments.

- Targeted Forgiveness Initiatives: Beyond PSLF, there have been efforts to forgive loans for borrowers defrauded by institutions, those with permanent disabilities, and specific cohorts under certain conditions.

The ongoing debate surrounding these programs highlights a fundamental tension: how to make higher education accessible and affordable without burdening taxpayers or creating moral hazard. This tension will undoubtedly fuel the discussions and potential legislative actions that will define Student Loan Policy 2026.

Anticipated Legislative Changes for Student Loan Policy in 2026

Predicting legislative outcomes is inherently challenging, as it depends on the political climate, economic conditions, and public sentiment. However, several themes and specific proposals are likely to dominate discussions around Student Loan Policy 2026.

1. Revisions to Income-Driven Repayment (IDR) Plans

IDR plans have been a cornerstone of federal student loan policy, offering a safety net for borrowers struggling to make payments. However, they have also been criticized for their complexity, administrative burdens, and the potential for ballooning interest. In 2026, we could see significant efforts to:

- Simplify Enrollment and Administration: Streamlining the application and annual recertification process for IDR plans is a common goal across the political spectrum. This could involve automatic enrollment or data-sharing agreements with the IRS.

- Adjust Payment Formulas: The percentage of discretionary income used to calculate payments (currently 10-15% depending on the plan) could be revised. There might also be changes to how "discretionary income" is defined, potentially increasing the protected income threshold.

- Accelerate Forgiveness Timelines: While some IDR plans offer forgiveness after 20 or 25 years, there could be proposals to shorten these timelines, particularly for borrowers with smaller loan balances or those who have consistently struggled.

- Address Interest Accrual: A major critique of IDR plans is that interest can accrue faster than payments, leading to growing loan balances even while borrowers are making payments. Legislative solutions might include subsidizing unpaid interest or capping the amount of interest that can accrue.

2. Expansion or Contraction of Loan Forgiveness Programs

Loan forgiveness remains a highly contentious issue. While broad-based forgiveness has faced significant legal and political hurdles, targeted forgiveness programs may see adjustments in 2026.

- Public Service Loan Forgiveness (PSLF) Reform: Despite efforts to simplify PSLF, many eligible borrowers still face challenges. Expect proposals to further streamline eligibility requirements, clarify qualifying employment, and address common administrative errors. There might also be discussions about expanding the definition of "public service."

- Targeted Relief for Specific Professions: Beyond PSLF, there could be renewed interest in forgiveness programs for specific high-need professions, such as teachers, nurses, or doctors in underserved areas, as a means to address workforce shortages.

- Forgiveness for Low-Balance Borrowers: A potential area of bipartisan agreement could be forgiving small loan balances, which are often held by borrowers who struggled to complete their education or have lower earning potential.

- Institutional Accountability: As part of any forgiveness discussion, there’s likely to be a push for increased accountability for institutions that consistently produce poor outcomes for their students, potentially linking institutional performance to federal aid eligibility or requiring them to share in the cost of loan defaults.

3. Changes to Federal Student Loan Interest Rates

The methodology for setting federal student loan interest rates is often debated. Currently, rates are tied to the 10-year Treasury note, plus a fixed add-on. In 2026, we might see proposals to:

- Lower or Cap Interest Rates: Arguments for lower interest rates often center on making education more affordable and reducing the long-term burden on borrowers.

- Introduce Variable Rates: While less popular due to market volatility, some proposals might explore variable rates or a hybrid system.

- Refinancing Options: A perennial debate is whether federal borrowers should have the ability to refinance their loans at lower interest rates, similar to private market options. This could be a significant legislative push.

4. Reimagining the Role of Private Student Loans

While federal loans dominate the conversation, private student loans play a substantial role for many students. Student Loan Policy 2026 might see legislative efforts to:

- Increase Oversight and Consumer Protections: Given the fewer protections offered by private loans, there could be calls for stricter regulations on private lenders, including clearer disclosure requirements and more flexible repayment options in cases of hardship.

- Encourage Federal Loan Prioritization: Policies might be introduced to ensure students exhaust all federal loan options before turning to private loans, which often carry higher interest rates and fewer benefits.

5. Broader Higher Education Finance Reforms

Beyond specific loan programs, any discussion about Student Loan Policy 2026 is inextricably linked to the broader issues of college affordability and accountability.

- Tuition Control Measures: Some proposals might link federal funding to tuition rate increases, incentivizing institutions to keep costs down.

- Increased Pell Grant Funding: Expanding the Pell Grant program, which provides need-based aid that doesn’t need to be repaid, is often seen as a way to reduce reliance on loans.

- Outcomes-Based Funding: Shifting federal funding models to reward institutions based on student success metrics (e.g., graduation rates, post-graduation earnings) could be a focus.

Impact on Borrowers: Navigating the Evolving Landscape

The potential legislative changes in Student Loan Policy 2026 will have a multifaceted impact on different borrower groups.

Current Borrowers

For those already carrying student loan debt, the primary concerns will revolve around repayment terms, interest rates, and access to forgiveness programs.

- Repayment Plan Adjustments: If IDR plans are simplified or made more generous, existing borrowers could see lower monthly payments or faster paths to forgiveness. Conversely, stricter rules could increase financial strain.

- Refinancing Opportunities: The ability to refinance federal loans at lower rates would be a boon for many, potentially saving thousands over the life of the loan.

- PSLF Clarity: Improvements to PSLF would offer greater certainty and access to forgiveness for public servants who have often faced bureaucratic hurdles.

- Communication is Key: Borrowers must stay informed about official communications from their loan servicers and the Department of Education. Changes won’t happen overnight, but awareness will be crucial.

Future Borrowers (Prospective Students)

Prospective students considering higher education will need to evaluate how Student Loan Policy 2026 might affect their ability to finance their education.

- Affordability and Accessibility: If policies lead to lower tuition, increased grant aid, or more favorable loan terms, college could become more accessible and affordable.

- Borrowing Decisions: The availability of specific loan types, interest rates, and potential forgiveness pathways will heavily influence how much students decide to borrow and from whom.

- Career Planning: Forgiveness programs like PSLF can influence career choices, and any changes to these programs could shift students’ post-graduation plans.

Risk Factors and Considerations

- Political Gridlock: The highly partisan nature of student loan debates means that significant legislative reform can be challenging to achieve. Incremental changes through administrative actions might be more likely than sweeping congressional bills.

- Economic Conditions: Inflation, interest rates, and the overall job market will influence both the need for and the political feasibility of various student loan policies. A struggling economy might increase pressure for borrower relief, while a robust economy might shift focus to fiscal responsibility.

- Litigation: Any major policy changes, especially those involving broad-based forgiveness, could face legal challenges, potentially delaying or overturning implementation.

Strategies for Borrowers to Prepare for 2026

Regardless of the specific legislative outcomes, proactive measures can help borrowers navigate the evolving student loan landscape.

1. Stay Informed and Engaged

- Monitor Official Sources: Regularly check the Department of Education’s website (studentaid.gov), reputable financial news outlets, and congressional updates for information on proposed and enacted legislation.

- Understand Your Loans: Know whether you have federal or private loans, your interest rates, your current repayment plan, and your loan servicer. This fundamental knowledge is your starting point.

2. Optimize Your Current Repayment Strategy

- Review IDR Eligibility: If you have federal loans and are struggling, explore Income-Driven Repayment plans. Even if changes are coming, being on an IDR plan now can offer immediate relief and potentially count towards future forgiveness.

- Consider Consolidation: For federal loans, consolidation can simplify payments and make you eligible for certain IDR plans or PSLF. Be aware of the implications, such as restarting payment counts for forgiveness.

- Explore Refinancing (Private Loans): If you have private loans, or if federal interest rates remain high, consider refinancing with a private lender if you have good credit and can secure a lower interest rate. Be cautious, as this means losing federal loan protections.

3. Build a Financial Safety Net

- Emergency Fund: Having 3-6 months of living expenses saved can provide a buffer against unexpected changes in loan terms or personal financial circumstances.

- Budgeting: A clear understanding of your income and expenses will help you identify areas where you can save or allocate more towards loan payments if needed.

4. Advocate for Change

- Contact Representatives: Share your experiences and concerns with your elected officials. Personal stories can be powerful in shaping policy debates.

- Support Advocacy Groups: Organizations dedicated to student loan reform often provide ways for individuals to get involved and amplify their voices.

The Economic and Societal Implications

Beyond individual borrowers, Student Loan Policy 2026 has broader economic and societal implications. The sheer volume of student debt impacts consumer spending, homeownership rates, and entrepreneurship. Policies that alleviate this burden could stimulate economic growth, while those that exacerbate it could stifle it.

Moreover, the accessibility and affordability of higher education are critical for social mobility and maintaining a skilled workforce. Policies that make college more attainable for all socioeconomic backgrounds can reduce inequality and strengthen the nation’s human capital. Conversely, a system that perpetuates debt or creates barriers to education can have long-term negative consequences for society as a whole.

The debate around student loans is not just about finance; it’s about the value we place on education, the fairness of our economic system, and the future of our society.

Conclusion: Preparing for the Future of Student Loan Policy in 2026

The year 2026 promises to be a pivotal moment for student loan policy. While the exact legislative outcomes remain uncertain, the direction of travel is clear: there will be continued pressure to address the soaring costs of higher education and the burden of student debt. Whether this manifests as significant reforms to IDR plans, targeted forgiveness initiatives, or broader changes to how we fund post-secondary education, borrowers must be prepared.

Staying informed, actively managing your current loans, building financial resilience, and engaging in advocacy are all crucial steps. The future of Student Loan Policy 2026 will undoubtedly shape the financial futures of millions, and by understanding the potential changes and preparing proactively, borrowers can best position themselves to navigate this evolving landscape. The conversation around student loans is far from over, and 2026 will be a key chapter in its ongoing story.