Student Loan Forgiveness 2026: Navigating Federal Program Updates & Eligibility

Student Loan Forgiveness 2026: Navigating the Latest Federal Program Updates and Eligibility Requirements for 10,000 Borrowers

The landscape of student loan debt in the United States is continuously evolving, bringing with it both challenges and opportunities for millions of borrowers. As we look towards Student Loan Forgiveness 2026, understanding the latest federal program updates, eligibility requirements, and the potential impact on your financial future is more critical than ever. This comprehensive guide aims to demystify these complex topics, offering clarity and actionable insights for up to 10,000 borrowers who could benefit from these programs.

The promise of student loan forgiveness has been a beacon of hope for countless individuals burdened by educational debt. While the journey to widespread relief has been fraught with legislative debates, policy changes, and legal challenges, the federal government continues to implement and refine programs designed to alleviate this financial strain. For those anticipating Student Loan Forgiveness 2026, staying informed is paramount. This article will delve into the current state of federal student loan forgiveness initiatives, highlight key changes, and provide a roadmap for determining your eligibility.

The Evolving Landscape of Student Loan Forgiveness

Student loan debt has reached unprecedented levels, prompting calls for significant reforms and relief measures. The federal government has responded with a series of initiatives, some broad in scope and others highly targeted. Understanding the historical context and the reasons behind these evolving policies is crucial for grasping the current state of Student Loan Forgiveness 2026.

A Brief History of Federal Forgiveness Programs

Historically, federal student loan forgiveness programs have primarily targeted specific professions or circumstances. Programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plan forgiveness have been available for years. However, their complexities, strict eligibility criteria, and administrative hurdles often meant that only a fraction of eligible borrowers successfully received relief.

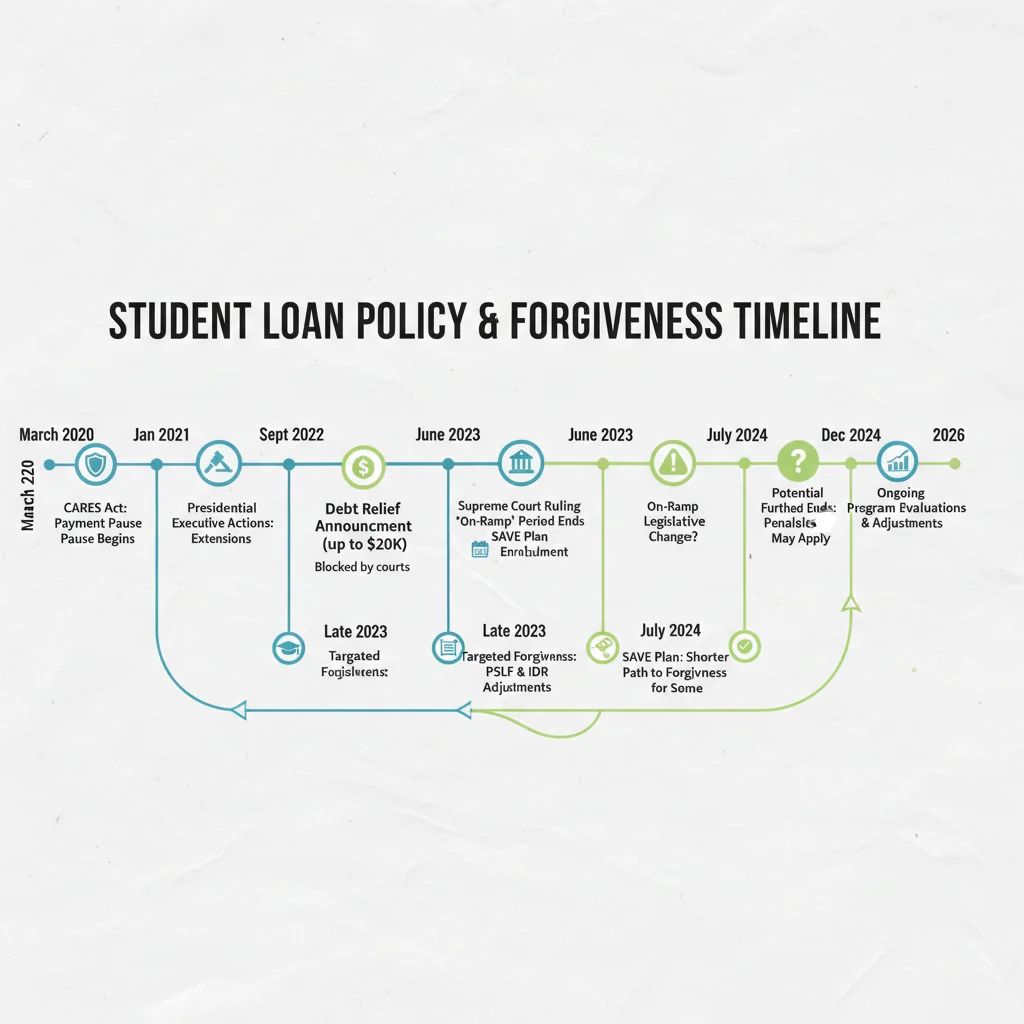

The COVID-19 pandemic brought about a temporary pause on federal student loan payments and interest, giving millions of borrowers a much-needed reprieve. This period also reignited discussions about broader student loan forgiveness, leading to new proposals and adjustments to existing programs. These changes are directly influencing what borrowers can expect from Student Loan Forgiveness 2026.

Recent Policy Shifts and Their Implications

In recent years, the Department of Education has undertaken significant efforts to address past administrative failures and expand access to existing forgiveness programs. This includes reviewing and adjusting IDR payment counts, making it easier for borrowers to qualify for PSLF, and providing targeted relief to specific groups, such as those defrauded by their institutions or those with total and permanent disabilities.

These policy shifts are not merely incremental; they represent a fundamental reevaluation of how federal student aid operates and how debt relief is administered. For borrowers looking ahead to Student Loan Forgiveness 2026, these changes could significantly alter their eligibility and the amount of relief they receive. It’s important to recognize that the government is actively working to streamline processes and ensure more borrowers receive the forgiveness they are entitled to under existing laws.

Key Federal Programs Relevant to Student Loan Forgiveness 2026

While a sweeping, universal student loan forgiveness program has faced legal and political obstacles, several federal initiatives continue to offer substantial relief. For Student Loan Forgiveness 2026, these programs will be the primary avenues for debt cancellation. Let’s explore them in detail.

Public Service Loan Forgiveness (PSLF)

PSLF remains a cornerstone of federal student loan relief. It forgives the remaining balance on Direct Loans after 120 qualifying monthly payments have been made under a qualifying repayment plan while working full-time for a qualifying employer. Qualifying employers include government organizations (federal, state, local, or tribal) and not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code.

- Eligibility: Must have Direct Loans, make 120 qualifying payments, and be employed full-time by a qualifying employer.

- Recent Updates: The Department of Education has made significant strides in correcting past errors and simplifying the PSLF process, including a limited PSLF Waiver that allowed past payments that previously didn’t count to be reconsidered. While the waiver period has largely ended, its impact continues to be felt, and future administrative adjustments could further ease the path to PSLF for Student Loan Forgiveness 2026.

- Actionable Steps: Ensure your employment is certified annually. Consolidate any Federal Family Education Loan (FFEL) Program loans or Perkins Loans into a Direct Consolidation Loan if you haven’t already.

Income-Driven Repayment (IDR) Plan Forgiveness

IDR plans are designed to make monthly student loan payments affordable based on a borrower’s income and family size. After a certain period of payments (typically 20 or 25 years, depending on the plan), any remaining loan balance is forgiven. The new Saving on a Valuable Education (SAVE) Plan is the latest and most generous IDR plan.

- The SAVE Plan: This plan offers lower monthly payments, prevents interest capitalization, and can lead to forgiveness in as little as 10 years for borrowers with original loan balances of $12,000 or less, with the forgiveness period extending for larger balances.

- IDR Account Adjustment: The Department of Education is conducting a one-time account adjustment to credit borrowers with more months toward IDR forgiveness, including periods of deferment and forbearance that previously didn’t count. This initiative is expected to bring millions of borrowers closer to forgiveness, potentially impacting Student Loan Forgiveness 2026 significantly.

- Actionable Steps: Enroll in an IDR plan, especially the SAVE Plan, if eligible. Ensure your income and family size information is updated annually.

Targeted Forgiveness Programs

Beyond PSLF and IDR, several other programs offer forgiveness for specific circumstances:

- Teacher Loan Forgiveness: Forgives up to $17,500 for eligible teachers who teach for five consecutive years in low-income schools.

- Total and Permanent Disability (TPD) Discharge: Forgives federal student loans for borrowers who are permanently disabled. The process has been streamlined, allowing for automatic discharge for those receiving Social Security disability benefits or verified by the Department of Veterans Affairs.

- Closed School Discharge: Forgives loans for students whose school closed while they were enrolled or shortly after they withdrew.

- Borrower Defense to Repayment: Provides relief to borrowers who were misled by their schools. The Department of Education has processed numerous claims, leading to billions in forgiveness.

These targeted programs will continue to be vital components of Student Loan Forgiveness 2026, offering relief to those who meet specific criteria.

Eligibility Requirements for Student Loan Forgiveness 2026

Determining your eligibility for Student Loan Forgiveness 2026 involves understanding the specific criteria for each program. While some general principles apply, the nuances of each initiative can significantly impact whether you qualify.

Loan Type Matters

The type of federal student loan you have is often the first and most critical factor. Generally, only Direct Loans are eligible for most forgiveness programs, including PSLF and the most generous IDR benefits. If you have older loan types, such as FFEL Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible.

Private student loans are typically not eligible for federal forgiveness programs. Borrowers with private loans must explore options offered by their private lenders, which are far less common.

Employment Verification for PSLF

For PSLF, your employment must be with a qualifying employer. This includes:

- Government organizations at any level (federal, state, local, or tribal).

- Not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code.

- Other not-for-profit organizations that provide certain public services.

It’s crucial to use the PSLF Help Tool to verify your employer’s eligibility and submit the Employment Certification Form annually or whenever you change employers. This proactive approach ensures your payments are being accurately tracked towards Student Loan Forgiveness 2026.

Income and Family Size for IDR Plans

Eligibility for IDR plans, including the SAVE Plan, is based on your discretionary income and family size. Your monthly payment is calculated as a percentage of your discretionary income. The lower your income relative to your family size, the lower your payments will be, and the faster you might reach forgiveness, especially under the SAVE Plan for smaller original loan balances.

You must recertify your income and family size annually. Failing to do so can result in higher payments or even removal from the IDR plan, delaying your path to Student Loan Forgiveness 2026.

Meeting Payment Requirements

For both PSLF and IDR forgiveness, you must make a specified number of qualifying payments. These payments must typically be:

- Made on time.

- For the full amount due.

- Under a qualifying repayment plan (for PSLF, this usually means an IDR plan).

The IDR account adjustment is a game-changer here, as it retroactively counts certain periods of deferment and forbearance towards forgiveness, potentially accelerating the timeline for many borrowers. This adjustment is particularly relevant for those seeking Student Loan Forgiveness 2026, as it could mean reaching the forgiveness threshold sooner than anticipated.

Strategies to Maximize Your Chances for Forgiveness

Navigating the complexities of federal student loan programs can be daunting, but with a strategic approach, you can significantly increase your chances of qualifying for Student Loan Forgiveness 2026. Here are key strategies to consider.

Understand Your Loan Portfolio

The first step is to know exactly what type of federal student loans you have. Log in to your Federal Student Aid (FSA) account at studentaid.gov to view your loan details. Identify whether you have Direct Loans, FFEL Program loans, or Perkins Loans. If you have older loan types, consider consolidation into a Direct Consolidation Loan to unlock eligibility for more programs.

Enroll in the Right Repayment Plan

For most forgiveness pathways, especially PSLF and IDR forgiveness, being on an income-driven repayment plan is essential. The SAVE Plan is currently the most beneficial for many borrowers due to its lower payment calculations and interest benefits. Evaluate your financial situation and enroll in the IDR plan that offers the lowest monthly payment while still counting towards forgiveness.

Certify Your Employment Annually (for PSLF)

If you are pursuing PSLF, do not wait until you have made 120 payments to certify your employment. Submit the PSLF Employment Certification Form annually and whenever you change employers. This ensures that your qualifying payments are being tracked correctly and helps prevent issues when you finally apply for forgiveness in Student Loan Forgiveness 2026 or beyond.

Stay Informed About Policy Changes

The federal student loan landscape is dynamic. New policies are introduced, and existing ones are refined. Regularly check official sources like studentaid.gov and subscribe to updates from the Department of Education. Being aware of changes, such as the IDR account adjustment or any new legislative proposals, can provide critical opportunities for accelerated forgiveness.

Keep Meticulous Records

Maintain thorough records of all your student loan documents, including:

- Loan statements.

- Payment confirmations.

- Employment certification forms.

- Correspondence with your loan servicer.

These records can be invaluable if there are discrepancies in your payment count or eligibility, especially as you approach Student Loan Forgiveness 2026.

Beware of Scams

Unfortunately, the promise of student loan forgiveness attracts scammers. Be wary of companies that charge fees for services you can get for free from your loan servicer or the Department of Education. Never share your FSA ID or password with anyone. All official communication about federal student loan programs will come from legitimate sources.

Anticipating Student Loan Forgiveness 2026: What to Expect

While definitive predictions are challenging, several factors suggest what borrowers might expect regarding Student Loan Forgiveness 2026. The current administration has shown a clear commitment to addressing student loan debt, primarily through existing statutory authority.

Continued Administrative Relief

Expect the Department of Education to continue its efforts to streamline and improve existing forgiveness programs. The IDR account adjustment is a prime example of administrative action that can provide significant relief without new legislation. More such adjustments or targeted initiatives could emerge, particularly as the department identifies further systemic issues.

The Impact of the SAVE Plan

The SAVE Plan is poised to be a major driver of Student Loan Forgiveness 2026. Its generous terms, including lower payments and accelerated forgiveness for smaller balances, mean that more borrowers will reach their forgiveness milestones in the coming years. Understanding and enrolling in this plan is crucial for many.

Potential for Further Legislative Action

While large-scale forgiveness proposals have faced hurdles, the political discourse around student debt relief is ongoing. Depending on future elections and legislative priorities, there could be renewed efforts to pass broader forgiveness measures. However, for Student Loan Forgiveness 2026, it’s safer to focus on current, enacted programs.

Focus on 10,000 Borrowers and Beyond

The goal of helping 10,000 borrowers, or many more, achieve forgiveness by 2026 is ambitious but achievable through the current pathways. The IDR account adjustment alone is expected to bring hundreds of thousands of borrowers closer to forgiveness, and continued engagement with PSLF and other programs will add to these numbers. The collective impact of these programs is designed to provide substantial relief to a significant portion of the student loan population.

Common Pitfalls to Avoid

Even with the best intentions, borrowers can make mistakes that delay or jeopardize their eligibility for student loan forgiveness. Being aware of these common pitfalls can help you navigate the process more smoothly towards Student Loan Forgiveness 2026.

Not Consolidating Older Loan Types

Many borrowers are unaware that older loan types, such as FFEL Program loans and Perkins Loans, may not qualify for PSLF or the most beneficial IDR plans unless they are consolidated into a Direct Consolidation Loan. Missing this step can lead to years of payments that don’t count towards forgiveness.

Failing to Certify Employment Annually for PSLF

For PSLF, timely employment certification is crucial. If you wait until you’ve made all 120 payments, and then discover an issue with your employer’s eligibility or your payment counts, it can be a lengthy and frustrating process to correct. Annual certification keeps your records up-to-date and helps identify problems early.

Not Recertifying Income for IDR Plans

IDR plans require annual recertification of your income and family size. If you miss this deadline, your payments can revert to a higher, non-income-driven amount, and any unpaid interest may capitalize, increasing your loan balance. This can also disrupt your progress toward IDR forgiveness.

Falling Victim to Scams

The student loan forgiveness space is unfortunately ripe for scams. Companies often promise guaranteed forgiveness for a fee or ask for sensitive personal information like your FSA ID. Remember, legitimate student loan help is free, and the Department of Education or your loan servicer are the only official sources of information and assistance.

Ignoring Your Loan Servicer Communications

It’s easy to ignore emails or letters from your loan servicer, but these communications often contain vital information about your loan status, repayment plan, and upcoming deadlines. Staying engaged with your servicer is key to remaining on track for Student Loan Forgiveness 2026.

Looking Ahead: The Future of Student Loan Debt and Forgiveness

The conversation around student loan debt is far from over. As we move closer to Student Loan Forgiveness 2026 and beyond, several trends and considerations will likely shape the future of federal student aid and debt relief.

Continued Focus on Affordability

There’s a growing consensus that higher education needs to be more affordable, and student loan repayment plans must be sustainable. Expect continued efforts to refine IDR plans and explore new mechanisms to prevent future generations from accumulating crushing debt burdens.

Data-Driven Policy Making

The Department of Education is increasingly using data to identify and address systemic issues within the student loan system. This data-driven approach could lead to more targeted interventions and automatic relief for certain groups of borrowers, further streamlining the path to forgiveness.

Addressing the Root Causes of Debt

While forgiveness provides relief, many policymakers and advocates are also focusing on addressing the root causes of student debt, such as rising tuition costs and inadequate state funding for higher education. Long-term solutions may involve a combination of debt relief, tuition reform, and increased grant funding.

Advocacy and Public Pressure

Student loan debt remains a significant political issue, and advocacy groups continue to push for broader relief. Public pressure will likely continue to play a role in shaping future policy decisions, potentially leading to new opportunities for Student Loan Forgiveness 2026 and beyond.

Conclusion

Student Loan Forgiveness 2026 is not a single, monolithic event but rather a culmination of existing federal programs, ongoing administrative reforms, and potential future policy adjustments. For the estimated 10,000 borrowers and many more who are navigating their student loan journey, understanding these pathways to relief is crucial.

By staying informed about the latest federal program updates, meticulously checking eligibility requirements, and proactively engaging with your loan servicer and the Department of Education, you can position yourself to take full advantage of available forgiveness opportunities. The path to debt relief may be complex, but with careful planning and consistent action, a future free from student loan burdens is within reach.

Remember to regularly visit studentaid.gov for the most accurate and up-to-date information directly from the source. Your financial well-being is a priority, and navigating the nuances of Student Loan Forgiveness 2026 effectively can make a substantial difference in achieving that goal.