Charitable Giving 2026: Optimize Deductions with QCDs & DAFs

In the evolving landscape of personal finance and philanthropy, strategic charitable giving has become more critical than ever. As we look ahead to 2026, understanding the nuances of tax-advantaged giving vehicles can significantly amplify your philanthropic impact while simultaneously optimizing your financial situation. This comprehensive guide delves into how you can optimize charitable giving in 2026, focusing on two powerful tools: Qualified Charitable Distributions (QCDs) and Donor-Advised Funds (DAFs).

The act of giving is inherently rewarding, but when coupled with intelligent financial planning, it can yield substantial tax benefits. The goal is to ensure that your generosity benefits not only the causes you care about but also your personal financial health. With potential changes in tax laws and economic conditions, staying informed about the best strategies for charitable contributions is paramount for every thoughtful donor.

The Evolving Landscape of Charitable Giving and Tax Deductions

Before diving into specific strategies, it’s essential to grasp the broader context of charitable giving. The Tax Cuts and Jobs Act (TCJA) of 2017 brought significant changes to itemized deductions, including those for charitable contributions. While the standard deduction increased substantially, fewer taxpayers found it advantageous to itemize. This shift made it more challenging for many to realize a direct tax benefit from their charitable donations.

However, even with these changes, opportunities to optimize charitable giving persist and, in some cases, have become even more attractive for specific donor profiles. For instance, individuals who are charitably inclined and have substantial assets, particularly in retirement accounts, can leverage strategies like QCDs and DAFs to make their giving more efficient and impactful.

Looking towards 2026, it’s crucial to consider that some provisions of the TCJA are set to expire. While predicting future tax legislation is always speculative, proactive planning based on current rules and potential changes is a hallmark of sound financial management. This article will focus on strategies that are robust under current law and likely to remain beneficial.

Why Optimize Your Charitable Giving?

- Maximize Impact: Ensure more of your money goes to the charity, not to taxes.

- Achieve Tax Efficiency: Reduce your taxable income or bypass tax liabilities altogether.

- Simplify Giving: Streamline your donation process and record-keeping.

- Plan for the Future: Establish a legacy of giving for years to come.

- Align with Financial Goals: Integrate philanthropy seamlessly into your broader financial and estate plans.

Understanding these benefits is the first step toward becoming a more strategic donor. The subsequent sections will break down how QCDs and DAFs serve as cornerstones of an effective plan to optimize charitable giving.

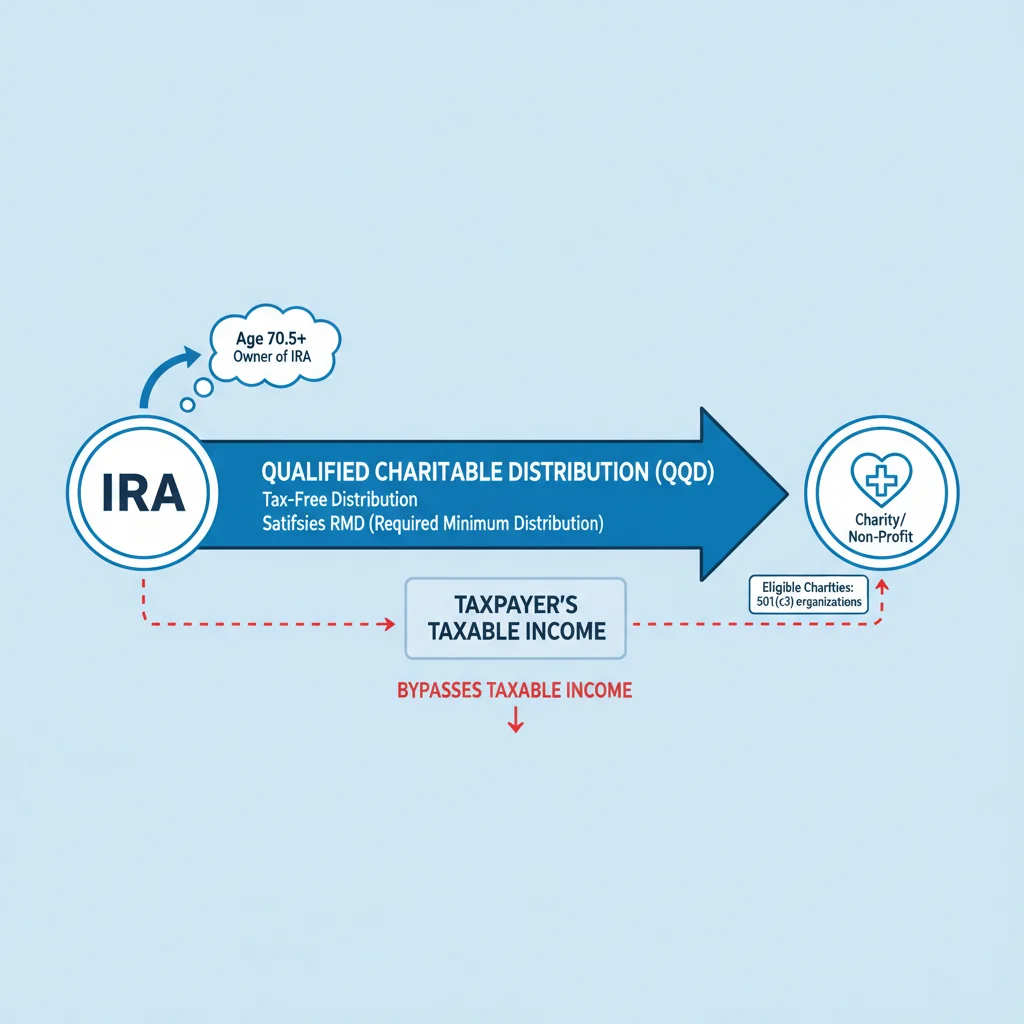

Qualified Charitable Distributions (QCDs): A Powerful Tool for Retirees

For individuals aged 70½ or older, a Qualified Charitable Distribution (QCD) stands out as an exceptionally tax-efficient way to make charitable donations directly from an Individual Retirement Account (IRA). This strategy is particularly valuable for those who no longer itemize deductions but still wish to support their favorite causes. By utilizing a QCD, you can directly transfer funds from your IRA to an eligible charity, with significant tax advantages.

How QCDs Work to Optimize Charitable Giving

A QCD allows you to distribute up to $100,000 per year (this amount is subject to indexing for inflation in future years, so always check current limits for 2026) directly from your IRA to a qualified charity. The key benefit? The amount distributed as a QCD is excluded from your gross income. This is a crucial distinction from taking a taxable distribution from your IRA and then donating the funds, which would only be deductible if you itemize.

Here’s a breakdown of the mechanics and benefits:

- Age Requirement: You must be 70½ or older at the time of the distribution.

- Direct Transfer: Funds must go directly from your IRA custodian to the charity. You cannot receive the funds first.

- Eligible Accounts: QCDs can be made from traditional IRAs, Roth IRAs, SEP IRAs, and SIMPLE IRAs, but only for contributions that would otherwise be taxable.

- Qualified Charities: The recipient must be a 501(c)(3) public charity. Donor-Advised Funds and private foundations are generally not eligible recipients for QCDs.

- Exclusion from Gross Income: This is the primary advantage. The distributed amount is not added to your adjusted gross income (AGI).

- Satisfies RMDs: For those aged 73 and older (or 72 if you turned 72 before January 1, 2023), QCDs count towards your Required Minimum Distribution (RMD) for the year. This is a significant benefit, as it allows you to fulfill your RMD obligation without increasing your taxable income.

The ability to satisfy your RMD without adding to your taxable income is a game-changer for many retirees. It can help keep your AGI lower, which in turn can impact other tax-related calculations, such as Medicare premiums, Social Security taxation, and eligibility for certain tax credits.

Who Benefits Most from QCDs to Optimize Charitable Giving?

- Non-Itemizers: If you take the standard deduction, a QCD allows you to receive a tax benefit for your charitable contribution that you wouldn’t otherwise get.

- High-Income Retirees: Those with substantial IRA balances who are subject to RMDs can use QCDs to manage their taxable income effectively.

- Individuals Concerned About AGI: A lower AGI can lead to reduced Medicare Part B and D premiums, lower taxes on Social Security benefits, and potentially qualify you for other tax breaks.

- Generous Donors: If you regularly give to charity, directing those donations through a QCD can make a significant difference to your tax bill.

Consider an example: Mary, aged 75, has an RMD of $15,000 this year. She also plans to donate $10,000 to her favorite animal shelter. If she takes the RMD as taxable income and then donates, she might not itemize, losing the tax benefit. However, if she makes a $10,000 QCD, that amount counts towards her RMD, reduces her taxable income by $10,000, and still fulfills her philanthropic goal. This is a clear way to optimize charitable giving.

Practical Steps for Implementing a QCD in 2026

- Contact Your IRA Custodian: Inform them of your intent to make a QCD. They will provide the necessary forms and guidance.

- Identify Eligible Charities: Ensure the charity is a 501(c)(3) public charity.

- Specify the Amount: Decide how much you want to donate, keeping the annual limit in mind.

- Ensure Direct Transfer: The check should be made payable to the charity and sent directly to them or to you for immediate forwarding to the charity (ensure the check is made out to the charity, not to you).

- Keep Records: Maintain thorough records of the QCD for tax purposes, including statements from your IRA custodian and acknowledgment letters from the charity.

By understanding and utilizing QCDs, retirees have a powerful avenue to not only support the causes they believe in but also to significantly enhance their personal tax planning. It’s a win-win strategy for those looking to optimize charitable giving in 2026 and beyond.

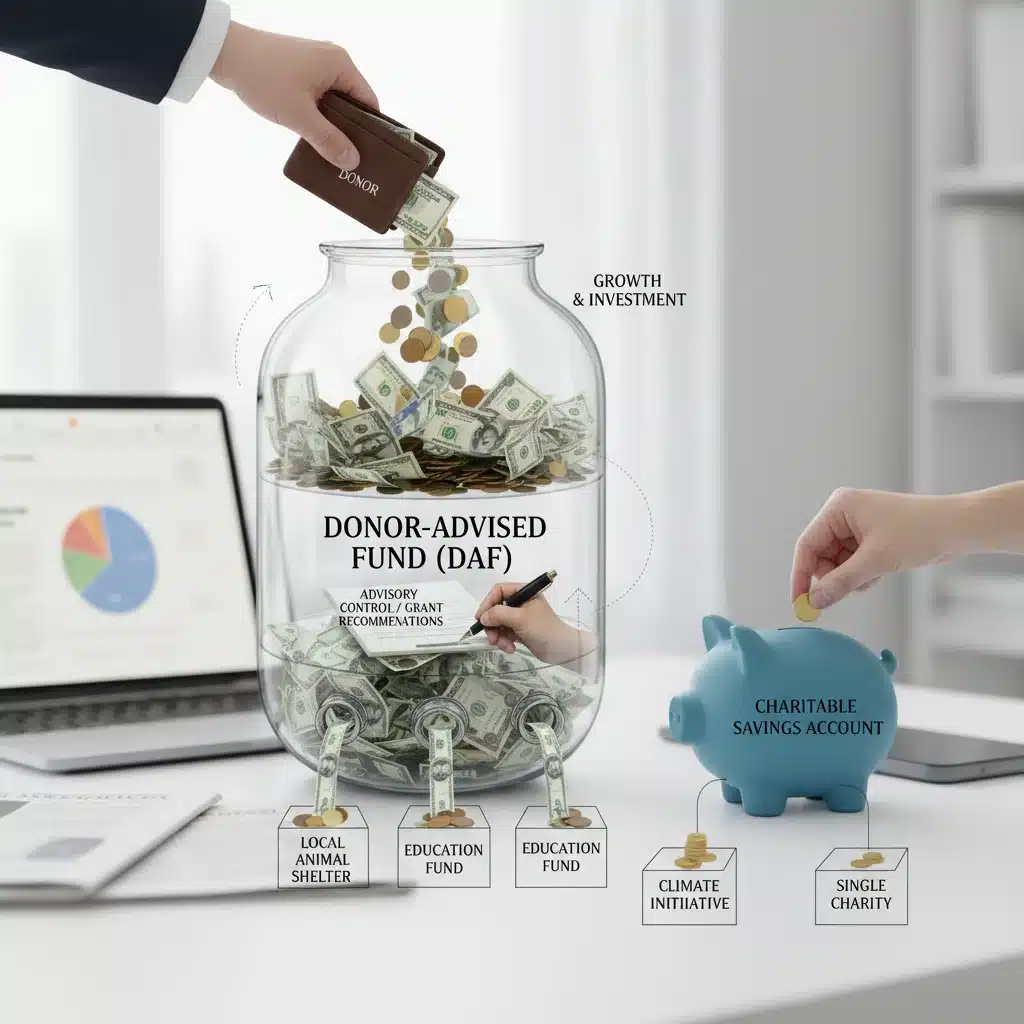

Donor-Advised Funds (DAFs): Flexibility and Strategic Giving

While QCDs are excellent for retirees making direct gifts from IRAs, Donor-Advised Funds (DAFs) offer a different, yet equally powerful, approach to optimize charitable giving for a broader range of donors. A DAF is essentially a charitable giving account established at a public charity (the sponsoring organization). It allows you to make an irrevocable contribution of cash, securities, or other assets to the fund, receive an immediate tax deduction, and then recommend grants from the fund to qualified charities over time.

The Mechanics of DAFs for Optimized Giving

When you contribute to a DAF, you are generally eligible for an immediate tax deduction in the year it’s made, regardless of when the grants to charities are distributed. The assets in the DAF can then be invested, potentially growing tax-free, and you can recommend grants from the fund to various charities at your own pace. This separation of the tax deduction from the actual distribution of funds to charities provides immense flexibility.

Key features and benefits of DAFs:

- Immediate Tax Deduction: You receive a deduction for your contribution in the year it’s made, regardless of when the grants to charities are distributed.

- Flexibility in Grantmaking: You can recommend grants to almost any IRS-qualified public charity at any time.

- Investment Growth: The assets in your DAF can be invested and grow tax-free, allowing for greater potential philanthropic impact.

- Anonymity (Optional): You can choose to make grants anonymously, which some donors prefer.

- Simplified Record-Keeping: The sponsoring organization handles all the administrative tasks, providing you with one single tax receipt for all your contributions to the DAF.

- Ideal for Lumpy Income: If you have a year with exceptionally high income (e.g., from a bonus, stock sale, or business liquidation), you can make a large contribution to a DAF to maximize your tax deduction in that year, then distribute funds to charities over several years.

- Legacy Planning: DAFs can be named with successor advisors, allowing your philanthropic legacy to continue beyond your lifetime.

DAFs are particularly effective for those who want to front-load their charitable deductions, especially in years where they can itemize, or when they have highly appreciated non-cash assets like stocks. Donating appreciated securities directly to a DAF allows you to avoid capital gains tax on the appreciation and still receive a deduction for the fair market value of the assets.

Who Benefits Most from DAFs to Optimize Charitable Giving?

- Donors with Appreciated Assets: Ideal for those wanting to donate stocks, mutual funds, or other securities, avoiding capital gains tax.

- High-Income Earners: Allows for a large deduction in a high-income year, even if you plan to distribute the funds to charities over many years.

- Strategic Planners: Provides a centralized hub for all charitable giving, simplifying administration and enabling a more thoughtful, long-term approach to philanthropy.

- Families: Can be used as a tool for family philanthropy, involving multiple generations in giving decisions.

- Those Who Itemize: DAF contributions are deductible as itemized charitable contributions.

For example, if John sells a highly appreciated stock in 2026, realizing a significant capital gain, he could contribute a portion of that stock directly to a DAF. He would avoid paying capital gains tax on the donated shares and receive an immediate income tax deduction for the fair market value of the stock. He could then recommend grants from his DAF to various charities over the next several years, without feeling rushed to make all his donations in one calendar year. This is a prime example of how DAFs help optimize charitable giving.

Establishing and Managing a DAF in 2026

- Choose a Sponsoring Organization: Major financial institutions (e.g., Fidelity Charitable, Schwab Charitable, Vanguard Charitable) and community foundations offer DAFs. Research their fees, investment options, and minimum contribution requirements.

- Fund Your DAF: Contribute cash, appreciated securities, or other assets. This is the point where you claim your tax deduction.

- Invest Your Funds: Select investment options for the assets within your DAF, allowing them to potentially grow tax-free.

- Recommend Grants: At any time, you can recommend grants to IRS-qualified public charities. The sponsoring organization performs due diligence and issues the grant.

- Keep Records: The sponsoring organization will provide statements for your contributions and grants.

DAFs provide an unparalleled level of flexibility and strategic advantage for donors who want to make a significant and lasting impact with their philanthropy. They are an indispensable tool for those looking to effectively optimize charitable giving.

Combining QCDs and DAFs for Ultimate Giving Optimization

While QCDs and DAFs are powerful on their own, for some individuals, a combination of both strategies can lead to even greater optimization. It’s important to note a critical distinction: QCDs cannot be made directly to DAFs. A QCD must go directly to a qualified public charity, and DAFs are generally considered sponsoring organizations, not direct charities for QCD purposes.

However, you can still use both in your overall financial and philanthropic plan. For instance, a retiree over 70½ could use QCDs to satisfy their RMDs by directing funds to charities that are not DAFs, thereby reducing their taxable income. Simultaneously, they could make separate contributions of appreciated securities or cash to a DAF from their non-IRA assets, receiving an itemized deduction for those contributions and setting up a flexible giving vehicle for future years.

Strategic Scenarios for Combined Use

- Scenario 1: RMD Management + Long-Term Giving: Use QCDs to meet RMDs tax-free, and fund a DAF with non-IRA assets (e.g., appreciated stock) for future, flexible giving and an immediate itemized deduction.

- Scenario 2: High-Income Year with RMD: In a year with high non-IRA income, make a large DAF contribution with cash or appreciated assets to maximize itemized deductions. Simultaneously, use a QCD to satisfy your RMD without adding to your taxable income.

- Scenario 3: Legacy Planning: Utilize QCDs for annual support of immediate causes, while the DAF is structured to create a lasting legacy for future generations to advise on charitable distributions.

The key is to understand the specific rules for each vehicle and how they can complement each other within your unique financial context. Consulting with a financial advisor and tax professional is highly recommended to tailor these strategies to your individual circumstances, especially as we plan for 2026.

Other Considerations for Optimizing Charitable Giving in 2026

Beyond QCDs and DAFs, several other factors and strategies can help you optimize charitable giving:

Donating Appreciated Non-Cash Assets

As mentioned with DAFs, donating appreciated securities (stocks, mutual funds) held for more than one year is often more tax-efficient than donating cash. If you donate appreciated stock, you generally avoid paying capital gains tax on the appreciation and can deduct the fair market value of the stock (up to certain AGI limits). This is a powerful strategy for both DAFs and direct gifts to public charities.

Bunching Charitable Contributions

Given the higher standard deduction, many taxpayers find it beneficial to "bunch" their charitable contributions. This involves combining several years’ worth of donations into a single year, allowing you to exceed the standard deduction threshold in that year and itemize, while taking the standard deduction in other years. A DAF is an excellent tool for bunching, as you can make a large contribution to the DAF in your "bunching year" (getting an immediate deduction) and then distribute grants from the DAF to charities over subsequent years.

State Tax Considerations

Remember that state tax laws also play a role. Some states offer their own charitable tax credits or deductions, which can further enhance the benefits of your giving. Researching your state’s specific provisions for 2026 can add another layer of optimization to your strategy.

Record-Keeping is Crucial

Regardless of the method you choose, meticulous record-keeping is non-negotiable. For cash donations, you’ll need bank records or written acknowledgments from the charity. For non-cash contributions, detailed records of the property, its value, and the charity’s acknowledgment are essential. For QCDs, keep statements from your IRA custodian and the charity’s acknowledgment. For DAFs, the sponsoring organization will provide comprehensive statements. Proper documentation is vital for claiming any tax benefits.

Understanding AGI Limitations

There are limits on how much you can deduct for charitable contributions based on your Adjusted Gross Income (AGI). For cash contributions to public charities, you can generally deduct up to 60% of your AGI. For appreciated property, it’s typically 30% of your AGI. Any excess contributions can usually be carried over for five subsequent tax years. Understanding these limits is important for maximizing your current year’s deduction and planning for future giving.

Looking Ahead to 2026: Proactive Planning is Key

As tax laws can change, it’s always advisable to plan proactively. While the core principles of QCDs and DAFs are well-established, specific limits and rules can be adjusted. Engaging with a qualified financial advisor and tax professional early in 2026 (or even in late 2025) will allow you to assess your personal financial situation, charitable goals, and the most current tax regulations. They can help you determine the optimal strategies to optimize charitable giving for your unique circumstances.

Whether your primary goal is to reduce your taxable income, fulfill your RMDs efficiently, simplify your giving process, or create a lasting philanthropic legacy, QCDs and DAFs offer powerful solutions. By leveraging these tools thoughtfully, you can ensure your generosity has the greatest possible impact, both for the causes you support and for your financial well-being.

In conclusion, charitable giving in 2026 presents numerous opportunities for optimization. By embracing strategies like Qualified Charitable Distributions for retirees and Donor-Advised Funds for flexible, strategic giving, individuals and families can make their philanthropic efforts more impactful and tax-efficient. This proactive approach not only benefits the charities but also empowers donors to align their values with their financial planning, creating a truly rewarding giving experience.