Retirement Account Tax Strategies 2026: Roth Conversions vs. Traditional IRA Deductions

Retirement planning is a journey that requires foresight, discipline, and a deep understanding of the financial landscape. As we look towards 2026, the intricacies of tax laws and investment vehicles become even more critical. For many, the central question revolves around how to best leverage retirement accounts to minimize tax burdens and maximize long-term savings. This comprehensive guide delves into the essential Retirement Tax Strategies for 2026, focusing specifically on the nuanced decisions between Roth conversions and traditional IRA deductions. Understanding these options is not just about saving money; it’s about building a robust financial future.

Retirement Account Tax Strategies 2026: Navigating Roth Conversions and Traditional IRA Deductions for Optimal Savings

The year 2026 brings with it a unique set of considerations for retirement savers. With potential shifts in tax legislation and the ever-present goal of financial security, making informed decisions about your retirement accounts is paramount. This article aims to demystify complex tax concepts, providing clear insights into Roth conversions and traditional IRA deductions, and helping you determine the most advantageous path for your individual circumstances. We will explore the benefits, drawbacks, and optimal scenarios for each strategy, ensuring you are well-equipped to make intelligent choices regarding your Retirement Tax Strategies.

Understanding the Core: Traditional IRAs and Roth IRAs

Before diving into the strategic comparisons, it’s crucial to grasp the fundamental differences between Traditional IRAs and Roth IRAs. These two retirement vehicles, while both offering tax advantages, operate on fundamentally different principles regarding when those tax advantages are realized.

Traditional IRA: Deductions Now, Taxes Later

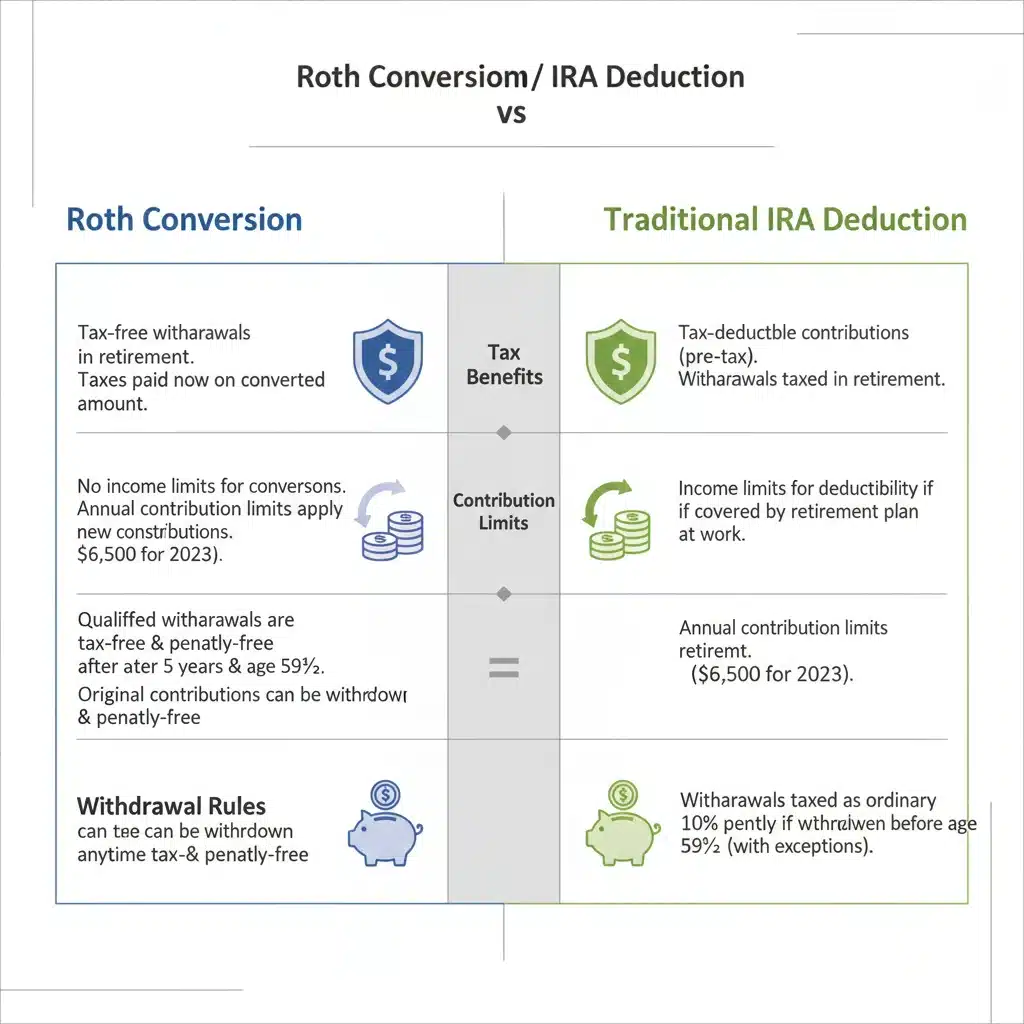

A Traditional IRA allows eligible individuals to contribute pre-tax dollars, meaning your contributions may be tax-deductible in the year they are made. This deduction can lower your taxable income in the present, which is particularly attractive if you expect to be in a lower tax bracket in retirement than you are currently. The money in a Traditional IRA grows tax-deferred, meaning you don’t pay taxes on the investment gains until you withdraw the funds in retirement. However, all qualified withdrawals in retirement are taxed as ordinary income. Required Minimum Distributions (RMDs) typically begin at age 73 (as of the SECURE 2.0 Act), forcing you to start withdrawing and paying taxes on your savings.

Roth IRA: Taxes Now, Tax-Free Later

In contrast, a Roth IRA is funded with after-tax dollars. This means your contributions are not tax-deductible in the year they are made. The trade-off, however, is significant: all qualified withdrawals in retirement are completely tax-free. This includes both your contributions and any investment earnings. This makes the Roth IRA an incredibly powerful tool for those who anticipate being in a higher tax bracket during retirement, or who simply prefer the certainty of knowing their retirement income will be tax-free. Roth IRAs also do not have RMDs for the original owner, providing greater flexibility in managing your distributions.

Traditional IRA Deductions for 2026: Who Benefits Most?

Deciding whether to take advantage of Traditional IRA deductions for 2026 hinges on several factors, primarily your current income level, your expected future income level, and your overall tax strategy. The primary benefit of a Traditional IRA is the upfront tax deduction. This can immediately reduce your taxable income, potentially pushing you into a lower tax bracket for the current year. For example, if you contribute $6,500 to a Traditional IRA and are in the 24% tax bracket, that deduction could save you $1,560 in taxes right away.

Eligibility for Deductibility

It’s important to note that the deductibility of Traditional IRA contributions can be phased out or eliminated if you (or your spouse) are covered by a retirement plan at work and your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds. For 2026, these thresholds are subject to adjustment, so staying informed about the latest IRS guidelines is crucial. If you are not covered by a workplace retirement plan, your contributions are generally fully deductible, regardless of your income.

When Traditional IRA Deductions Shine

- Higher Current Income: If you are currently in a high tax bracket, the immediate tax deduction offered by a Traditional IRA can be very appealing. It effectively defers taxes until retirement, when you might be in a lower tax bracket.

- Anticipated Lower Retirement Income: If you expect your income to be significantly lower in retirement, paying taxes on withdrawals at that time might result in a lower overall tax burden than paying taxes on contributions today.

- Need for Upfront Tax Savings: For individuals or families who need to reduce their current tax liability, the Traditional IRA deduction provides an immediate financial benefit.

- Catch-Up Contributions: If you are age 50 or older, you can make additional catch-up contributions to a Traditional IRA, further increasing your potential deduction.

However, the downside is that every dollar you withdraw in retirement from a Traditional IRA will be subject to income tax. This can be a concern if tax rates rise in the future or if your retirement income turns out to be higher than anticipated, potentially pushing you into a higher tax bracket than you are in today. This uncertainty is a key factor when considering your Retirement Tax Strategies.

The Power of Roth Conversions: A Forward-Looking Strategy

A Roth conversion involves moving funds from a Traditional IRA (or other pre-tax retirement accounts like a 401(k)) into a Roth IRA. The key implication of a Roth conversion is that you pay taxes on the converted amount in the year of the conversion. While this might seem counterintuitive to pay taxes now, it unlocks the significant benefit of tax-free withdrawals in retirement. This strategy is a cornerstone of advanced Retirement Tax Strategies for many individuals.

Why Consider a Roth Conversion in 2026?

The decision to undertake a Roth conversion is often driven by a belief that current tax rates are lower than future tax rates, or a desire for predictable tax-free income in retirement. Here are some scenarios where a Roth conversion makes strategic sense:

- Anticipated Higher Future Tax Rates: If you believe tax rates are likely to increase in the future, paying taxes on your retirement savings at today’s potentially lower rates can be a smart move.

- Expected Higher Retirement Income: If you anticipate a high income in retirement from other sources (pensions, Social Security, other investments), having a portion of your retirement savings be tax-free can significantly reduce your overall tax burden.

- Long Time Horizon Until Retirement: The longer your money has to grow tax-free in a Roth IRA, the more beneficial a conversion becomes. The tax-free growth compounds over many years, leading to substantial tax savings.

- No RMDs for Original Owner: Roth IRAs do not have RMDs for the original owner, offering greater flexibility in managing your distributions and preserving your capital for longer, or for legacy planning for heirs.

- Estate Planning Benefits: Roth IRAs can be excellent estate planning tools. Heirs typically receive tax-free withdrawals, and the absence of RMDs for the original owner means the account can continue to grow tax-free for their benefit for a period.

- Temporary Dip in Income: If you experience a year with unusually low income (e.g., career break, business loss), this can be an opportune time to perform a Roth conversion, as you’ll pay taxes on the conversion at a lower rate.

The Tax Implications of a Roth Conversion

When you convert funds from a Traditional IRA to a Roth IRA, the amount converted (minus any non-deductible contributions you’ve made to the Traditional IRA) is added to your taxable income for the year of the conversion. This can significantly increase your tax bill for that year. Therefore, it’s crucial to have funds available to pay these taxes, ideally from sources outside of your retirement accounts, to avoid reducing your retirement savings.

It’s also important to be aware of the five-year rule for Roth conversions. While your original contributions to a Roth IRA can be withdrawn tax-free and penalty-free at any time, converted amounts must generally remain in the Roth IRA for at least five years (and you must be at least 59½ years old) for qualified withdrawals to be tax-free and penalty-free. Violating this rule can lead to taxes and penalties on the converted amount.

Comparing Roth Conversions and Traditional IRA Deductions for 2026

The choice between prioritizing Traditional IRA deductions and performing Roth conversions is not a one-size-fits-all decision. It requires a careful analysis of your current financial situation, your future expectations, and your risk tolerance regarding tax rates. Let’s break down the comparison to help you craft your optimal Retirement Tax Strategies for 2026.

When Traditional IRA Deductions Might Be Superior

- Higher Current Tax Bracket, Lower Expected Retirement Tax Bracket: If you are currently in your peak earning years and anticipate a significant drop in income and thus a lower tax bracket in retirement, the immediate tax deduction of a Traditional IRA is highly advantageous. You save taxes at your current high rate and pay taxes at a lower rate later.

- Uncertainty About Future Tax Rates: If you are unsure whether tax rates will be higher or lower in the future, deferring taxes with a Traditional IRA keeps your options open. You can always convert to a Roth later if circumstances change.

- Need for Current Tax Savings: If you are looking to reduce your current tax bill to free up cash flow or invest in other areas, the Traditional IRA deduction provides that immediate benefit.

- Income Above Roth IRA Contribution Limits: If your MAGI is too high to directly contribute to a Roth IRA, a Traditional IRA might still be an option for deductible contributions (depending on workplace plan coverage).

When Roth Conversions Might Be Superior

- Lower Current Tax Bracket, Higher Expected Retirement Tax Bracket: If you are currently in a lower tax bracket (e.g., early career, temporary unemployment, or a year with lower income), converting to a Roth IRA allows you to pay taxes on the conversion at a reduced rate, securing tax-free growth and withdrawals in what might be a higher future tax bracket.

- Belief in Rising Future Tax Rates: If you are confident that tax rates will increase significantly in the future, a Roth conversion is a proactive move to lock in your tax rate today.

- Desire for Tax-Free Retirement Income: For those who prioritize predictable, tax-free income in retirement, a Roth IRA is unparalleled. This eliminates concerns about future tax law changes impacting your retirement withdrawals.

- Estate Planning: As mentioned, Roth IRAs offer superior estate planning benefits, allowing heirs to inherit tax-free income.

- No RMDs: The absence of RMDs provides ultimate flexibility in managing your retirement assets, allowing them to grow tax-free for as long as you wish.

Key Considerations for Your Retirement Tax Strategies in 2026

Beyond the direct comparison, several other factors should influence your Retirement Tax Strategies for 2026.

1. Your Age and Time Horizon

The younger you are, the more time your Roth IRA has to grow tax-free, making a Roth conversion potentially more valuable. Conversely, if you are nearing retirement, the immediate tax deduction of a Traditional IRA might be more impactful, or a Roth conversion might be considered if you have a specific short-term tax advantage (e.g., a low-income year) and enough non-retirement funds to pay the conversion taxes.

2. Your Income Level and Tax Bracket

Your current and projected tax brackets are perhaps the most significant determinants. A high current income often favors Traditional IRA deductions, while a low current income (especially if you expect higher income later) makes Roth conversions more appealing. Be mindful of the MAGI limits for direct Roth IRA contributions and Traditional IRA deductibility.

3. Availability of Funds for Conversion Taxes

If you plan a Roth conversion, ensure you have sufficient non-retirement funds to pay the taxes on the converted amount. Paying taxes from the converted funds themselves reduces the amount that can grow tax-free, diminishing the strategy’s effectiveness.

4. Future Tax Law Changes

Tax laws are not static. While we plan for 2026, future legislative changes could impact the attractiveness of either strategy. Staying informed and being flexible in your planning is crucial. Many financial experts anticipate that current tax rates might be historically low, suggesting future increases, which would favor Roth strategies.

5. Required Minimum Distributions (RMDs)

For those concerned about RMDs, a Roth conversion can be a powerful tool to reduce or eliminate them. By converting Traditional IRA assets to a Roth IRA, those assets are no longer subject to RMDs for the original owner, providing greater control over your retirement income stream and potentially reducing your taxable income in later life.

6. Backdoor Roth IRA

For high-income earners who exceed the MAGI limits for direct Roth IRA contributions, the “backdoor Roth IRA” strategy remains a viable option. This involves making a non-deductible contribution to a Traditional IRA and then immediately converting it to a Roth IRA. While the contribution isn’t deductible, the conversion of the after-tax funds is typically tax-free (assuming no other pre-tax IRA funds). This is a sophisticated strategy that requires careful execution, especially if you have existing pre-tax IRA balances, due to the pro-rata rule.

7. Pro-Rata Rule for Roth Conversions

If you have multiple Traditional IRA accounts, and some contain pre-tax funds while others contain non-deductible (after-tax) funds, the IRS’s pro-rata rule applies to Roth conversions. This rule states that if you convert only a portion of your IRA funds, you cannot simply convert the after-tax portion tax-free. Instead, the conversion is treated as coming proportionally from all your Traditional IRA accounts (pre-tax and after-tax). This can lead to a larger taxable event than anticipated if not properly understood and planned for. This is a critical detail in advanced Retirement Tax Strategies.

Developing Your Personalized Retirement Tax Strategies for 2026

Given the complexity and the significant financial implications, developing your Retirement Tax Strategies for 2026 should ideally involve professional guidance. A qualified financial advisor or tax professional can help you:

- Analyze Your Current and Projected Financial Situation: They can assess your income, expenses, assets, and liabilities to build a comprehensive financial picture.

- Estimate Future Tax Brackets: Using various economic models and your personal projections, they can help you estimate your likely tax bracket in retirement.

- Model Different Scenarios: A good advisor can run projections comparing the long-term impact of Traditional IRA deductions versus Roth conversions on your overall wealth and tax liability.

- Navigate Tax Laws and Rules: They stay updated on the latest tax legislation, including potential changes for 2026 and beyond, and understand intricate rules like the pro-rata rule and five-year rule.

- Integrate with Overall Financial Plan: Retirement account decisions should not be made in isolation. An advisor can help integrate these strategies into your broader financial plan, including investments, estate planning, and risk management.

- Optimize Timing: The timing of a Roth conversion can be just as important as the decision to convert. An advisor can help identify opportune moments, such as low-income years or periods of market downturns.

Remember, the goal is not just to minimize taxes in any single year, but to optimize your tax position over your entire lifetime, ensuring your retirement savings are as robust and accessible as possible. This holistic approach is the hallmark of effective Retirement Tax Strategies.

Conclusion: Making Informed Decisions for Your Retirement Future

As you plan for retirement in 2026 and beyond, the choices you make regarding your Traditional IRA deductions and potential Roth conversions will have a profound impact on your financial well-being. Both strategies offer unique advantages, and the optimal path depends entirely on your individual circumstances, financial goals, and outlook on future tax rates. Whether you prioritize immediate tax savings or tax-free income in retirement, understanding these options is the first step towards securing a comfortable and tax-efficient future.

Take the time to thoroughly evaluate your situation, consider the long-term implications of each decision, and don’t hesitate to seek expert advice. By proactively engaging with these Retirement Tax Strategies, you can build a more resilient and prosperous retirement nest egg, giving you peace of mind and financial freedom in your golden years.

The landscape of retirement planning is ever-evolving, but with careful consideration and strategic planning, you can navigate the complexities of tax laws and make choices that serve your best interests for decades to come. The future of your financial security starts with the decisions you make today.