Build Your 6-Month Emergency Fund by 2026: A Comprehensive 5-Step Guide

In an unpredictable world, financial security is not just a luxury; it’s a necessity. One of the cornerstones of a robust financial plan is a well-funded emergency fund. This isn’t just about having some extra cash; it’s about creating a safety net substantial enough to cover life’s unexpected twists and turns without derailing your long-term financial goals. Our mission for you, by 2026, is to establish a solid emergency fund 2026 that can cover six months of your essential living expenses. This comprehensive guide will walk you through five actionable steps to achieve this crucial financial milestone.

The year 2026 might seem a little far off, but when it comes to building significant financial reserves, time is your greatest ally. Starting now allows you to implement a gradual, sustainable approach, making the process less stressful and more achievable. Whether it’s a sudden job loss, an unexpected medical bill, a major home repair, or a car breakdown, an emergency fund provides the peace of mind that you can handle these situations without resorting to high-interest debt or compromising your future.

Many people struggle with where to begin, or how to maintain momentum once they start. This guide aims to demystify the process, breaking it down into manageable steps. We’ll cover everything from calculating your target amount to optimizing your savings strategies and ensuring your fund is easily accessible yet protected. By following these steps, you’ll be well on your way to securing your financial future and achieving the goal of a 6-month emergency fund 2026.

Step 1: Calculate Your Target Emergency Fund Amount

The first and most critical step in building your emergency fund 2026 is to clearly define your financial target. How much money do you actually need? The widely accepted benchmark is to have three to six months’ worth of essential living expenses saved. For our purpose, we are aiming for the more robust six-month target. This provides a greater buffer against longer periods of unemployment or multiple unexpected events.

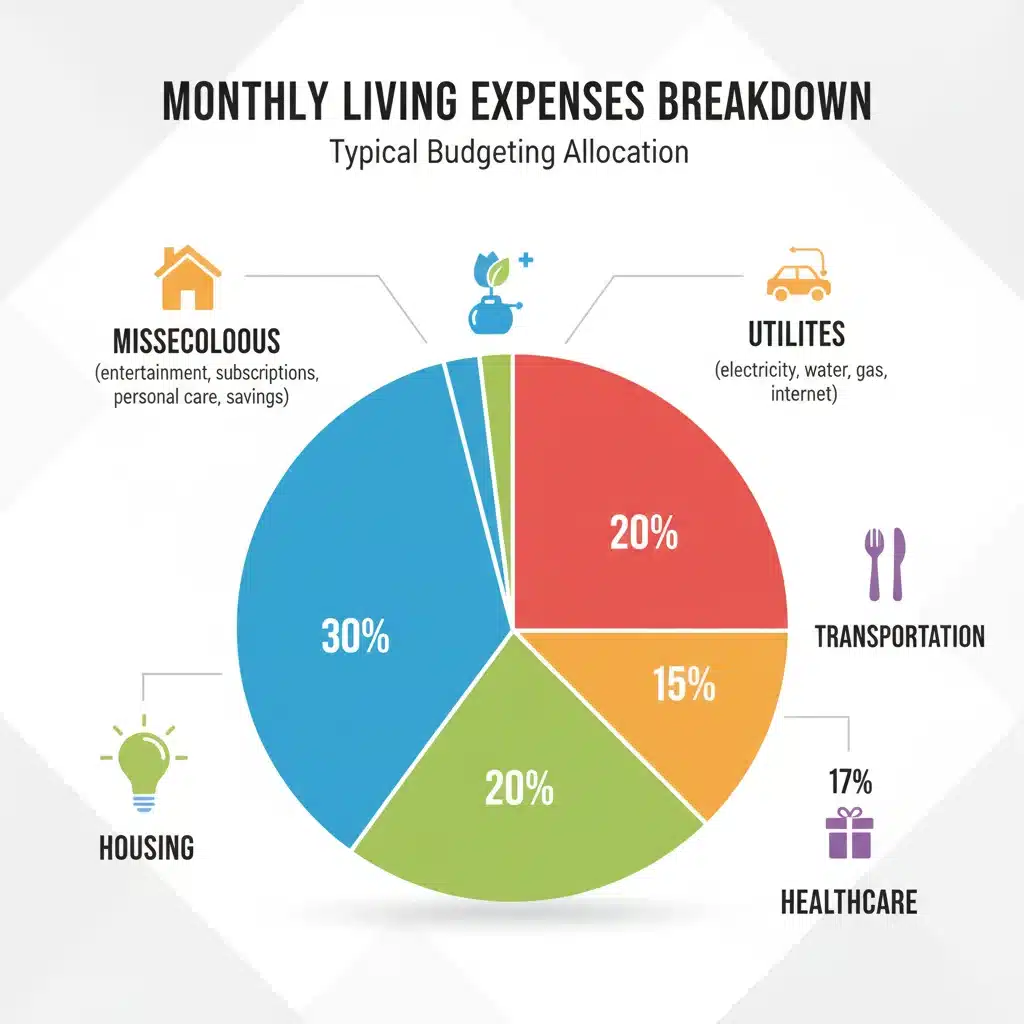

Identify Your Essential Living Expenses

To calculate this, you need to differentiate between essential and non-essential expenses. Essential expenses are those you absolutely cannot live without. These typically include:

- Housing: Rent or mortgage payments, property taxes, homeowner’s insurance.

- Utilities: Electricity, gas, water, internet (often considered essential in today’s world).

- Food: Groceries, not dining out.

- Transportation: Car payments, fuel, public transport costs, car insurance, basic maintenance.

- Healthcare: Health insurance premiums, essential medications.

- Minimum Debt Payments: Student loan minimums, credit card minimums (though ideally, you’d pay more, the emergency fund focuses on survival).

Non-essential expenses, which you would cut in an emergency, include:

- Dining out, entertainment, vacations, subscriptions you don’t use regularly, new clothes, gym memberships (if you can exercise at home).

The Calculation Process

- Track Your Spending: For at least one month, meticulously track every dollar you spend. Use a budgeting app, a spreadsheet, or even a notebook. This gives you a realistic picture of your actual outgoings.

- Categorize Expenses: Separate your tracked expenses into essential and non-essential categories.

- Sum Essential Expenses: Add up all your essential monthly expenses. Let’s say this total comes to $3,000.

- Multiply by Six: To get your target emergency fund 2026 amount, multiply your essential monthly expenses by six. In our example, $3,000 x 6 = $18,000. This is your target.

Be honest and realistic with your numbers. Overestimating your essential expenses slightly is better than underestimating. Remember, this fund is for survival, not for maintaining your current lifestyle during a crisis. This concrete number will serve as your guiding star throughout the entire process of building your emergency fund 2026.

Step 2: Create a Realistic Budget and Find Savings Opportunities

Once you know your target, the next step is to figure out how you’re going to get there. This involves a deep dive into your current financial situation through budgeting and actively seeking out areas where you can save more. A well-constructed budget is your roadmap to financial success, especially when aiming for a significant goal like a 6-month emergency fund 2026.

Budgeting Fundamentals

There are several budgeting methods you can employ, but the core principle remains the same: understand where your money is coming from and where it’s going. Popular methods include:

- 50/30/20 Rule: Allocate 50% of your income to needs (essentials), 30% to wants (non-essentials), and 20% to savings and debt repayment. This is a great starting point, but you might need to adjust the percentages to prioritize your emergency fund 2026.

- Zero-Based Budgeting: Every dollar has a job. You allocate every cent of your income to an expense or a savings goal. This method is highly effective for maximizing savings but requires more effort.

- Envelope System: For cash spenders, this involves allocating physical cash into envelopes for different spending categories.

Choose a method that resonates with you and stick to it. Consistency is key.

Identifying Savings Opportunities

This is where you get proactive about freeing up cash for your emergency fund 2026. Look at both your essential and non-essential spending with a critical eye.

Cutting Non-Essential Expenses:

- Subscription Services: Audit all your streaming services, gym memberships, apps, and other recurring subscriptions. Cancel anything you don’t use regularly or can live without for a while.

- Dining Out/Takeaway: This is often one of the biggest budgetbusters. Commit to cooking more at home. Even cutting back by a few meals a week can free up significant funds.

- Entertainment: Look for free or low-cost entertainment options. Libraries, public parks, free community events, and home-based hobbies can replace expensive outings.

- Shopping: Implement a ‘no-spend’ challenge for a week or a month, or simply be more mindful of impulse purchases. Ask yourself if you truly need something before buying it.

Optimizing Essential Expenses:

Even essentials can often be reduced:

- Groceries: Plan your meals, make a list, and stick to it. Buy generic brands, look for sales, and avoid shopping when hungry. Consider meal prepping to reduce waste and temptation.

- Utilities: Be mindful of energy consumption. Unplug electronics, turn off lights, adjust your thermostat. Look into energy-efficient alternatives.

- Insurance: Shop around for better rates on car, home, and health insurance. Sometimes bundling policies can offer discounts.

- Transportation: Can you carpool, use public transport more often, or bike/walk for shorter distances? Even small changes can add up.

- Debt Interest: While you’re building your emergency fund, focus on minimum payments, but once it’s established, aggressively tackle high-interest debt. For now, try to avoid taking on new debt.

Increase Your Income (If Possible)

While cutting expenses is crucial, increasing your income can significantly accelerate your progress towards your emergency fund 2026 target. Consider:

- Side Hustles: Freelancing, ride-sharing, food delivery, selling crafts, tutoring, or offering services based on your skills.

- Selling Unused Items: Declutter your home and sell items you no longer need on platforms like eBay, Facebook Marketplace, or local consignment shops.

- Ask for a Raise: If you’re performing well at your job, prepare a case for a raise.

- Overtime: If available and manageable, consider picking up extra hours at work.

Every extra dollar you earn and save brings you closer to your emergency fund 2026 goal. Be creative and consistent in finding ways to boost your income.

Step 3: Automate Your Savings and Choose the Right Account

One of the most powerful strategies for consistent saving is automation. By setting up automatic transfers, you remove the temptation to spend the money and ensure steady progress towards your emergency fund 2026. Equally important is choosing the right place to store your fund.

Automate Your Contributions

Treat your emergency fund contributions like a non-negotiable bill. Set up an automatic transfer from your checking account to your dedicated emergency savings account immediately after you get paid. Even if it’s a small amount to start, consistency builds momentum.

- Frequency: Choose weekly, bi-weekly, or monthly transfers, aligning with your pay schedule.

- Amount: Start with an amount you know you can consistently afford, even if it’s just $25 or $50. As you find more savings or increase income, bump up this amount.

- Pay Yourself First: The philosophy here is simple: allocate money to your savings before you allocate it to spending. This ensures your financial goals are prioritized.

Choosing the Right Account

Where you keep your emergency fund 2026 is crucial. It needs to be:

- Accessible: You need to be able to get to the money quickly if an emergency arises, typically within 1-3 business days.

- Separate: It should be in an account separate from your everyday checking account to avoid accidental spending. Out of sight, out of mind (from a spending perspective).

- Safe: It must be FDIC-insured (in the US) or covered by similar government deposit insurance in your country. This protects your money even if the bank fails.

- Earning Interest: While the primary goal isn’t growth, your money should at least keep pace with inflation as much as possible.

Given these criteria, the best option for an emergency fund 2026 is typically a high-yield savings account (HYSA).

- High-Yield Savings Accounts (HYSAs): These are offered by online banks and typically provide significantly higher interest rates than traditional brick-and-mortar bank savings accounts. They are FDIC-insured, easily accessible through online transfers, and separate from your daily spending.

- Money Market Accounts: Similar to HYSAs, they often offer competitive interest rates and check-writing privileges, though they might have minimum balance requirements.

- Avoid Investing: Do NOT put your emergency fund into the stock market or other volatile investments. While these offer higher potential returns, they also carry a risk of losing principal, which defeats the purpose of an emergency fund. This money needs to be stable and safe.

Research different online banks to find the HYSA that offers the best interest rate with no monthly fees and easy transfer options. This dedicated account will be the home for your growing emergency fund 2026.

Step 4: Stay Motivated and Track Your Progress

Building a significant emergency fund takes time and discipline. It’s easy to lose steam, especially when progress feels slow. Therefore, staying motivated and consistently tracking your progress are vital for reaching your emergency fund 2026 goal.

Visualizing Your Progress

Humans are visual creatures. Seeing your progress can be incredibly motivating:

- Savings Tracker: Create a visual tracker – a thermometer, a bar graph, or even a simple spreadsheet where you color in squares as you hit milestones. Post it somewhere you’ll see it daily.

- Digital Tools: Many budgeting apps and banking platforms offer visual representations of your savings goals. Utilize these features.

- Milestone Rewards: Set small, non-financial rewards for yourself when you hit certain milestones (e.g., 1 month saved, 3 months saved). This could be a special treat, a new book, or a fun experience that doesn’t derail your savings.

Regularly Review Your Budget and Goals

Your financial situation isn’t static, and neither should your budget be. Review your budget and your emergency fund 2026 progress at least monthly:

- Adjust as Needed: Have your expenses changed? Did you get a raise? Adjust your savings contributions accordingly. If you’re consistently exceeding your savings goal, increase your automatic transfer amount. If you’re struggling, re-evaluate your expenses.

- Reaffirm Your ‘Why’: Remind yourself why you’re building this fund. Is it for peace of mind? To protect your family? To avoid debt? Keeping your motivation strong is crucial.

- Celebrate Small Wins: Acknowledge every deposit, every extra dollar saved. These small victories contribute to the larger goal of your emergency fund 2026.

Avoid Dipping into the Fund Prematurely

This is perhaps the hardest part. Once you’ve started accumulating a substantial amount, it can be tempting to use it for non-emergencies. Remember the strict definition of an emergency:

- True Emergencies: Job loss, unexpected medical bills, urgent home repairs (e.g., burst pipe, furnace breakdown), car repairs that prevent you from getting to work.

- Not Emergencies: A sale on a new TV, a last-minute vacation, holiday shopping, a desire for a new gadget.

If you do have to use your emergency fund 2026, make a plan to replenish it as quickly as possible. Treat it as if you borrowed from yourself and need to pay it back.

Step 5: Maintain and Strengthen Your Emergency Fund Beyond 2026

Reaching your goal of a 6-month emergency fund 2026 is a monumental achievement, but the journey doesn’t end there. Financial security is an ongoing process. This final step focuses on maintaining your fund and considering how to further strengthen your financial resilience.

Regular Reviews and Adjustments

Even after 2026, continue to review your emergency fund at least annually, or whenever there’s a significant life change:

- Cost of Living Adjustments: Has your cost of living increased? Have essential expenses like rent, groceries, or insurance premiums gone up? Adjust your target fund amount accordingly to ensure it still covers six months of current expenses.

- Life Changes: A new job, a new baby, a home purchase, or a change in health status can all impact your essential expenses and the level of financial cushion you need. Recalculate your target and replenish or add to your fund as required.

- Inflation: Over time, inflation erodes the purchasing power of money. While a high-yield savings account helps, it’s essential to ensure your fund remains adequate in real terms.

Consider a Tiered Approach (After Reaching the 6-Month Goal)

Once your initial 6-month emergency fund 2026 is fully funded and stable, you might consider a tiered approach to your emergency savings, especially if you have complex financial situations or higher-risk careers:

- Tier 1: Core Emergency Fund (6 months): Kept in a high-yield savings account, easily accessible. This is what you’ve worked so hard for.

- Tier 2: Extended Emergency/Opportunity Fund (beyond 6 months): For those who want an even larger buffer (e.g., 9-12 months) or want to save for foreseeable large expenses (e.g., a new roof, car replacement). This portion might be in a slightly less liquid but still safe vehicle, like a Certificate of Deposit (CD) that matures in a year or two, or potentially even a very low-risk bond fund, though this introduces some market risk. The key is that this is *after* your primary 6-month fund is secured.

The goal is to maintain the liquidity and safety of your core emergency fund while optimizing any excess for slightly better returns if your risk tolerance allows and your financial situation is robust.

Financial Planning Beyond the Emergency Fund

The discipline and habits you build while creating your emergency fund 2026 will serve you well in other areas of financial planning. Once the fund is complete, redirect those automatic savings contributions to other financial goals:

- Retirement Savings: Maximize contributions to your 401(k), IRA, or other retirement accounts.

- Debt Repayment: Aggressively pay down high-interest debt like credit cards or personal loans.

- Investment Goals: Save for a down payment on a home, a child’s education, or other significant investments.

- Wealth Building: Explore diversified investment strategies to grow your net worth.

Your fully funded emergency fund is a launchpad for these next financial adventures, providing a stable foundation from which to build wealth and achieve even greater financial freedom.

Common Pitfalls to Avoid When Building Your Emergency Fund

While the steps seem straightforward, many people encounter obstacles. Being aware of these common pitfalls can help you navigate them successfully on your path to a robust emergency fund 2026.

1. Underestimating Essential Expenses

One of the biggest mistakes is not accurately calculating your essential monthly expenses. People often forget sporadic but necessary costs like annual insurance premiums, car registration, or certain medical co-pays. When calculating, try to average these annual costs into a monthly figure. A precise number is critical for your emergency fund 2026 target.

2. Lack of Automation

Relying solely on willpower to save is a recipe for inconsistency. If you wait until the end of the month to see what’s left to save, there often isn’t much. Automating your savings to transfer immediately after payday ensures that your financial goals are prioritized. Make saving for your emergency fund 2026 non-negotiable.

3. Treating it as a ‘Savings Account’ for Anything

The emergency fund is distinct from general savings. It’s not for a down payment on a car, a vacation, or a new gadget. It’s solely for unexpected, unavoidable emergencies. Dipping into it for non-emergencies undermines its purpose and leaves you vulnerable when a real crisis hits. Keep it sacred.

4. Keeping it in an Inaccessible or Low-Interest Account

Parking your emergency fund in a regular checking account makes it too easy to spend. Conversely, putting it in an investment that ties up funds or exposes it to market volatility is also problematic. A high-yield savings account strikes the perfect balance of accessibility, safety, and modest growth.

5. Getting Discouraged by Slow Progress

Building a 6-month emergency fund, especially if you’re starting from scratch, takes time. It’s a marathon, not a sprint. Don’t get discouraged if you’re not seeing massive leaps in your balance overnight. Focus on consistency. Every small contribution adds up. Celebrate mini-milestones to keep motivation high for your emergency fund 2026.

6. Not Adjusting for Life Changes

Life is dynamic. Your expenses can change due to new jobs, family additions, or changes in housing. Failing to recalculate and adjust your emergency fund target can leave you underprepared. Make it a habit to review your fund’s adequacy annually or after significant life events.

7. Not Having a Plan to Replenish

If you do have to use your emergency fund for a legitimate crisis, it’s crucial to have a plan to rebuild it quickly. Treat it like a loan you’ve taken from yourself. Prioritize replenishing the fund before resuming other discretionary spending or long-term investment goals.

The Psychological Benefits of a Fully Funded Emergency Fund

Beyond the tangible financial security, having a fully funded emergency fund 2026 offers profound psychological benefits that are often overlooked but incredibly valuable.

Reduced Stress and Anxiety

Financial worries are a leading cause of stress for many individuals and families. The constant fear of the unknown – what if I lose my job? What if the car breaks down? – can be debilitating. An emergency fund acts as a powerful antidote to this anxiety. Knowing you have a financial cushion to fall back on provides immense peace of mind, allowing you to focus on other aspects of your life without the shadow of impending financial doom.

Increased Confidence and Control

When unexpected events occur, they can often make you feel helpless. With an emergency fund, you regain a sense of control. You’re not at the mercy of credit card companies or desperate measures. This control translates into increased confidence in your ability to handle life’s challenges, knowing you’ve proactively prepared for them. This empowers you to make decisions from a position of strength, not desperation.

Better Decision-Making

Without an emergency fund, a sudden job loss might force you to take the first job offer that comes along, even if it’s not the right fit or pays less than you deserve. An emergency fund gives you the luxury of time. You can take a few extra weeks or months to find a job that aligns with your career goals and pays what you’re worth. Similarly, for unexpected expenses, you can make informed decisions about repairs or medical treatments without being pressured by immediate financial constraints.

Freedom from High-Interest Debt

One of the most insidious traps during an emergency is resorting to high-interest credit card debt or payday loans. This can quickly spiral out of control, creating a long-term financial burden that far outweighs the initial emergency. Your emergency fund 2026 is your shield against this debt cycle, preserving your credit score and your future financial health.

Enhanced Overall Well-being

The cumulative effect of reduced stress, increased confidence, and better decision-making contributes to a significant improvement in your overall well-being. You’ll likely sleep better, have fewer arguments about money, and feel more optimistic about your future. This sense of well-being is an invaluable return on your investment in building your emergency fund 2026.

Conclusion: Your Path to Financial Resilience by 2026

Building a 6-month emergency fund 2026 is more than just a financial goal; it’s a commitment to your future self and your peace of mind. It’s a strategic move that transforms financial vulnerability into financial resilience. By meticulously following these five steps – calculating your target, budgeting and finding savings, automating your contributions, staying motivated, and maintaining your fund – you are laying a robust foundation for enduring financial security.

Remember, the journey might have its challenges, but the rewards are profound. The discipline you cultivate, the financial literacy you gain, and the profound sense of security you achieve will empower you to face life’s inevitable uncertainties with confidence and calm. Don’t delay; start today. Every dollar saved brings you closer to that vital 6-month cushion. By 2026, you’ll look back at this decision as one of the best financial moves you ever made, having built a powerful safeguard against whatever the future may hold. Your financial freedom begins with your emergency fund 2026.