IDR Account Adjustment: How Millions of Borrowers Could See Loan Balances Reduced by 2026

IDR Account Adjustment: How Millions of Borrowers Could See Loan Balances Reduced by 2026

For millions of student loan borrowers across the United States, the burden of debt has been a persistent cloud. However, a significant ray of hope has emerged in the form of the IDR Account Adjustment, a policy change poised to reduce loan balances for a substantial number of individuals by 2026. This comprehensive adjustment aims to correct past administrative errors and ensure that borrowers receive proper credit for time spent in repayment, ultimately leading to earlier loan forgiveness for many. Understanding the intricacies of this initiative is crucial for any borrower seeking to navigate their student loan journey effectively.

The IDR Account Adjustment, often referred to as the ‘Payment Count Adjustment’ or ‘IDR Waiver,’ is a one-time initiative by the U.S. Department of Education. Its primary goal is to address historical inaccuracies in the tracking of payments made under Income-Driven Repayment (IDR) plans and certain forbearances. For years, many borrowers found themselves making payments for extended periods without seeing their loan balances decrease or receiving accurate credit towards forgiveness timelines. This adjustment seeks to rectify those issues, ensuring that eligible borrowers receive the credit they deserve, potentially leading to loan forgiveness much sooner than they anticipated.

This article will delve deep into the IDR Account Adjustment, explaining its purpose, who stands to benefit, the types of loans and repayment periods covered, and the critical steps borrowers need to take to ensure they receive the maximum benefit. We will also explore the potential impact on your financial future and what to expect as the adjustment rolls out over the coming years. If you have student loans, particularly federal ones, understanding this adjustment is not just beneficial – it could be life-changing.

Understanding the Core of the IDR Account Adjustment

At its heart, the IDR Account Adjustment is about fairness and accuracy. The Department of Education recognized that its previous systems for tracking payments and periods of deferment or forbearance were flawed. These flaws often resulted in borrowers not receiving credit for time that should have counted towards their 20 or 25-year IDR forgiveness timelines. The adjustment is designed to retroactively count certain periods of repayment, as well as specific types of deferment and forbearance, that previously did not qualify.

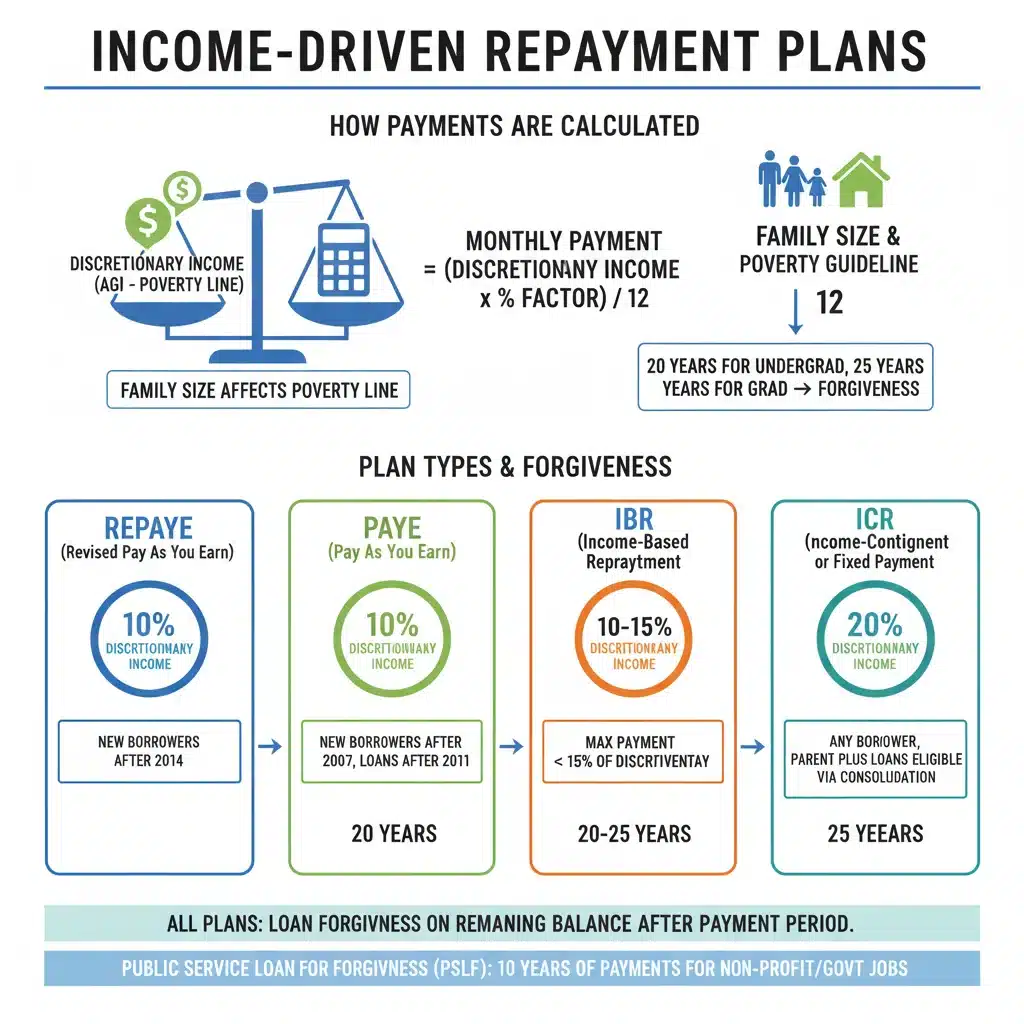

What is an Income-Driven Repayment (IDR) Plan?

Before diving deeper into the adjustment, it’s essential to understand IDR plans themselves. Income-Driven Repayment plans are federal student loan repayment options designed to make loan payments more manageable by capping them at a percentage of your discretionary income. After a certain period (typically 20 or 25 years, depending on the plan and when you borrowed), any remaining loan balance is forgiven. The four main IDR plans are:

- Revised Pay As You Earn (REPAYE): Generally 10% of discretionary income.

- Pay As You Earn (PAYE): Generally 10% of discretionary income, but never more than the 10-year Standard Repayment Plan amount.

- Income-Based Repayment (IBR): Generally 10% or 15% of discretionary income, depending on when you borrowed.

- Income-Contingent Repayment (ICR): The lesser of 20% of discretionary income or what you’d pay on a fixed 12-year plan adjusted by your income.

The promise of these plans is eventual forgiveness, but inconsistent tracking and communication often left borrowers confused about their progress. The IDR Account Adjustment aims to clarify and accelerate this progress.

Why Was the Adjustment Needed?

The need for the IDR Account Adjustment stemmed from several systemic issues:

- Inconsistent Payment Tracking: Loan servicers sometimes failed to accurately track qualifying payments, leading to discrepancies in borrowers’ records.

- Misapplication of Forbearance: Some servicers aggressively pushed borrowers into long-term forbearances, even when IDR plans would have been more beneficial. These forbearance periods often did not count towards forgiveness.

- Lack of Communication: Borrowers often weren’t fully informed about their IDR progress or the implications of certain repayment statuses.

- Administrative Complexity: The sheer complexity of federal student loan programs, with multiple loan types and repayment options, made consistent application of rules challenging.

These issues resulted in many borrowers effectively ‘losing credit’ for years of repayment or non-payment that, under a more equitable system, should have counted towards their forgiveness timeline. The IDR Account Adjustment is a direct response to these long-standing problems.

Who Benefits from the IDR Account Adjustment?

The potential beneficiaries of the IDR Account Adjustment are vast, encompassing millions of federal student loan borrowers. While the exact number of borrowers who will achieve full forgiveness or a reduced balance will become clearer as the adjustment is fully implemented, the eligibility criteria are broad.

Eligible Loan Types

Primarily, the adjustment applies to federally held student loans, which include:

- Direct Loans (subsidized, unsubsidized, PLUS, and consolidation loans).

- Federal Family Education Loan (FFEL) Program loans held by the Department of Education.

- Perkins Loans held by the Department of Education.

Crucially, if you have commercially held FFEL Program loans or Perkins Loans, you must consolidate them into a Direct Consolidation Loan by April 30, 2024, to benefit from this adjustment. This deadline is critical, as consolidation allows these older loan types to become eligible for the new counting rules.

Eligible Repayment Periods That Will Now Count

The most significant aspect of the IDR Account Adjustment is the expansion of what counts as a qualifying payment period. The following periods will now be credited towards IDR forgiveness, even if they weren’t previously:

- Any month in which a borrower was in repayment status, regardless of the payment amount or loan type. This is a major change, as historically, only payments made specifically under an IDR plan counted.

- 12 or more months of consecutive forbearance: If you had 12 or more consecutive months in forbearance, those months will now count.

- 36 or more months of cumulative forbearance: If you had 36 or more cumulative months in forbearance (even if not consecutive), those months will now count.

- Certain periods in deferment: This includes deferments before 2013 (excluding in-school deferment), and economic hardship deferment.

- Any time in repayment prior to consolidation: If you consolidated your loans, all periods of repayment on the underlying loans prior to consolidation will now count towards the IDR forgiveness timeline of the new Direct Consolidation Loan. This is particularly beneficial for those who consolidated multiple times.

These expanded criteria mean that many borrowers who thought they were far from forgiveness might suddenly find themselves much closer, or even eligible for immediate forgiveness.

The Mechanics of the IDR Account Adjustment: How It Works

The process of implementing the IDR Account Adjustment is largely automatic for most eligible borrowers. However, understanding the timeline and what to expect is important.

Automatic Implementation for Many

For borrowers with Direct Loans or federally held FFEL Program loans, the Department of Education will automatically review their accounts. The review process involves analyzing historical data from loan servicers and the National Student Loan Data System (NSLDS) to identify all periods that now qualify for credit under the new rules. Once this review is complete, the updated payment counts will be applied to borrowers’ accounts.

The Importance of Consolidation

As mentioned, if you have commercially held FFEL Program loans, Perkins Loans, or Health Education Assistance Loan (HEAL) Program loans, you absolutely must consolidate them into a Direct Consolidation Loan by April 30, 2024. Failure to do so means these loans will not benefit from the IDR Account Adjustment. Consolidation combines multiple federal loans into a single new loan with one interest rate (a weighted average of your previous rates) and one monthly payment. More importantly for this adjustment, it makes older loan types eligible for the new, more generous payment counting rules.

Timeline for Implementation and Notification

The Department of Education began implementing the IDR Account Adjustment in phases. Borrowers who reach the necessary 20 or 25 years of qualifying payments (240 or 300 months) as a result of the adjustment are among the first to receive notifications of forgiveness. These notifications began in late 2023 and continue into 2024. For those who don’t immediately qualify for forgiveness but see a significant increase in their payment counts, updates to their loan accounts will be reflected by 2026. This phased approach allows the Department to process millions of accounts systematically.

What Happens After the Adjustment?

- Loan Forgiveness: If your updated payment count reaches the 240 or 300 months required for IDR forgiveness, your remaining loan balance will be discharged, and you will be notified.

- Reduced Balance: If you don’t reach full forgiveness, your payment count will be updated, bringing you closer to your forgiveness date. This means fewer payments will be required in the future.

- Refunds: In some cases, if the adjustment puts you over the required number of payments for forgiveness, you might be eligible for a refund of payments made beyond the forgiveness threshold. This is more common for those who have been in repayment for a very long time.

Key Steps Borrowers Should Take Now

While much of the IDR Account Adjustment is automatic, there are critical steps you can take to ensure you benefit fully and to track your progress.

1. Determine Your Loan Types

Log in to StudentAid.gov to check your loan types. This is paramount. If you have any commercially held FFEL Program loans, Perkins Loans, or HEAL loans, you must consolidate them into a Direct Consolidation Loan by April 30, 2024. This is a hard deadline for these older loan types to receive the full benefit of the adjustment.

2. Consider Consolidation Even for Direct Loans

Even if you have only Direct Loans, consolidation might be beneficial in specific scenarios. If you have multiple Direct Loans with different repayment histories, consolidating them can result in the highest payment count being applied to the new consolidated loan. For example, if you have one loan with 100 qualifying payments and another with 50, consolidating them could mean the new loan gets credit for 100 payments, rather than starting fresh or having separate counts. This strategy is particularly useful if you have older loans with more repayment history. Always consider the pros and cons, as consolidating resets your Public Service Loan Forgiveness (PSLF) count (though the IDR adjustment will count past periods). However, for IDR this is generally a net positive.

3. Ensure You Are on an IDR Plan or Enroll in One

While the adjustment counts past periods regardless of your current plan, to continue making progress towards forgiveness after the adjustment, you should be enrolled in an Income-Driven Repayment (IDR) plan. If you are not currently on an IDR plan, or if your plan is outdated, visit StudentAid.gov to apply for or switch to an eligible IDR plan. The new SAVE Plan (Saving on a Valuable Education) is often the most generous option for many borrowers.

4. Check Your Loan History and Records

Periodically review your loan history on StudentAid.gov. While the Department of Education is performing the adjustments, it’s always wise to be informed. You can download your loan data to see your repayment history, deferments, and forbearances. If you believe there are errors or missing periods, keep records of your payments and communications with servicers.

5. Stay Informed

The Department of Education continues to release updates on the IDR Account Adjustment. Regularly check StudentAid.gov, subscribe to their email updates, and follow reputable financial news sources. This is an evolving process, and staying informed will help you make timely decisions.

Impact and Future Outlook of the IDR Adjustment

The IDR Account Adjustment represents one of the most significant overhauls of the federal student loan system in recent history. Its impact is projected to be profound, offering relief to millions.

Massive Loan Forgiveness and Balance Reductions

The Department of Education estimates that hundreds of thousands of borrowers will achieve immediate loan forgiveness as a direct result of this adjustment. Millions more are expected to see a substantial reduction in the time remaining until their loans are forgiven. This translates to less financial stress, more disposable income, and greater financial mobility for a significant portion of the population.

Addressing Historical Inequities

Beyond the financial relief, the adjustment directly addresses long-standing criticisms of the federal student loan system regarding its complexity and the inconsistent application of rules. It acknowledges that borrowers were often disadvantaged by administrative failures, and it seeks to right those wrongs. This move builds trust and provides a more equitable path to student loan forgiveness.

Economic Implications

The widespread reduction or elimination of student loan debt can have broader economic benefits. Borrowers with less debt are more likely to pursue homeownership, start businesses, save for retirement, and contribute to the economy in other ways. This stimulus can have a ripple effect, boosting consumer spending and overall economic growth.

Long-Term Changes to Loan Servicing

The IDR Account Adjustment also serves as a catalyst for improved loan servicing practices. The scrutiny and the need to implement this complex adjustment are pushing servicers and the Department of Education to develop more robust and transparent tracking systems. Future borrowers should benefit from a more streamlined and accurate experience when it comes to tracking their progress towards IDR forgiveness.

Potential Challenges and Considerations

While overwhelmingly positive, the implementation of such a massive adjustment is not without its challenges. Borrowers may experience delays in updates to their accounts, and some may need to proactively follow up with their servicers if they believe their counts are incorrect. It is crucial for borrowers to remain vigilant and informed throughout this process.

Frequently Asked Questions (FAQs) About the IDR Account Adjustment

Q1: Is the IDR Account Adjustment the same as the PSLF Waiver?

No, while both were one-time adjustments addressing past issues, they are distinct. The Public Service Loan Forgiveness (PSLF) Waiver focused on expanding eligibility for PSLF by counting previously ineligible payments. The IDR Account Adjustment focuses on correcting IDR payment counts for all federal loan borrowers, regardless of employment, and includes crediting certain periods of deferment and forbearance. However, for those pursuing PSLF, the IDR adjustment can also add qualifying payments towards their 120 PSLF payments, making it beneficial for both IDR and PSLF hopefuls.

Q2: Do I need to apply for the IDR Account Adjustment?

For most borrowers with Direct Loans or federally held FFEL Program loans, the adjustment is automatic, and no application is needed. However, if you have commercially held FFEL Program loans, Perkins Loans, or HEAL loans, you must consolidate them into a Direct Consolidation Loan by April 30, 2024, to receive the benefit. This is the only ‘application’ step required for certain loan types.

Q3: What if I already consolidated my loans? Will I still benefit?

Yes! The IDR Account Adjustment is particularly beneficial for borrowers who have consolidated. It will count periods of repayment on the underlying loans (the loans you consolidated) prior to consolidation towards the IDR forgiveness timeline of your new Direct Consolidation Loan. This means your payment count won’t reset to zero, as it would have under previous rules. If you consolidated multiple times, the Department of Education will look back at all periods of repayment on all underlying loans.

Q4: How will I know if my loans have been adjusted or forgiven?

The Department of Education will notify you if your loans are forgiven or if your payment count has been updated significantly. You should also regularly check your loan servicer’s website and StudentAid.gov for updates to your account. Forgiveness notifications began in late 2023 and continue into 2024, with all eligible accounts expected to be updated by 2026.

Q5: What is the deadline to consolidate commercially held FFEL loans?

The critical deadline to consolidate commercially held FFEL Program loans, Perkins Loans, or HEAL loans into a Direct Consolidation Loan to receive the benefits of the IDR Account Adjustment is April 30, 2024.

Q6: Will I pay taxes on the forgiven amount?

Under the American Rescue Plan Act of 2021, student loan forgiveness through December 31, 2025, is federal tax-free. This means that any loan amount forgiven due to the IDR Account Adjustment during this period will not be considered taxable income by the IRS. However, state tax laws vary, so it’s advisable to check with your state’s tax authority or a tax professional regarding potential state tax implications.

Conclusion: A New Era for Student Loan Borrowers

The IDR Account Adjustment marks a pivotal moment for federal student loan borrowers. By rectifying past administrative oversights and providing credit for previously ineligible periods, this initiative offers a tangible path to reduced loan balances and, for many, outright forgiveness. The promise of millions seeing their loan burdens eased by 2026 is a testament to a commitment to a more equitable and understandable student loan system.

For borrowers, proactive engagement is key. While many aspects are automatic, understanding your loan types, considering consolidation if necessary, and staying informed about updates are crucial steps to maximizing the benefits. This adjustment is not just about numbers on a ledger; it’s about freeing individuals from decades of debt, empowering them to pursue their financial goals, and fostering a more stable economic future. The time to act and understand your eligibility is now, ensuring you don’t miss out on this historic opportunity for student loan relief.